Seamus Phelan

Life & Protection Team Leader

Cormac Logue

Life & Protection Department

Alan Broderick

Life & Protection Department

Colin Bailey

Life & Protection Department

Maik Ikponwen

Life & Protection Department

Conor O'Hare

Life & Protection Department

Aidan Butler

Life & Protection Department

Diarmuid Woods

Life & Protection Department

Colm Farrel

Life & Protection Department

David Heffernan

Life & Protection Department

Rebecca Lynch

Life & Protection Department

What is Multi Claim Protection Cover?

Multi-Claim Protection Cover is a simple and cost-effective life and illness protection policy. It is designed to provide financial support if you experience certain health conditions that could impact your ability to work or manage day-to-day life.

Unlike traditional protection policies, Multi Claim Protection allows you to make multiple claims over the lifetime of the policy, depending on the severity of the condition. Payments are linked to predefined health events, and the amount paid varies based on the severity of the illness or injury.

The level of cover and the conditions included can differ from one provider to another, which is why it is important to speak with one of our advisors before choosing a policy. They can help you understand how each option works and which one best suits your needs.

You can complete our easy-to-understand form for a free online quote comparison, or speak directly with one of our Qualified Financial Advisors who will guide you through the process and help you get the right cover.

Why is Multi Claim Protection Cover Different?

Multi-Claim Protection Cover is designed to provide financial support that reflects the severity of a medical condition and the impact it can have on your health, lifestyle, and ability to work.

With many traditional serious illness policies, a claim is usually paid once after diagnosis. Once the claim is paid, the cover typically ends, meaning you may not be able to take out the same type of protection again.

Multi-Claim Protection Cover works differently. Even after making a claim for a significant health setback, your policy can continue, as long as you have not claimed 100% of the total cover available. This means you can still have financial protection in place for future health events that may affect your wellbeing and lifestyle.

What is health impacts are covered?

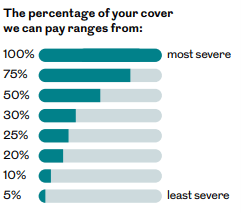

Multi-Claim Protection Cover is based on the severity of health setbacks rather than a single diagnosis. Claims are assessed according to how seriously a condition affects your health, recovery, and day-to-day life.

Cover typically includes a wide range of health events, from major serious illnesses such as cancer, heart attack, and stroke, to less severe but still impactful conditions that may require ongoing treatment or recovery time. Depending on the provider, cover can also extend to events such as long hospital stays, major surgeries, or injuries resulting from accidents, including traffic accidents.

The amount paid depends on the seriousness of the condition and how it is defined within the policy terms. Some conditions may trigger a partial payment, while more severe or life-changing illnesses can result in a higher percentage of the total cover being paid.

As cover definitions and payment levels can vary between providers, speaking with one of our advisors is important. They can explain what is included, how claims are assessed, and help you choose a policy that offers the right level of protection for your needs.

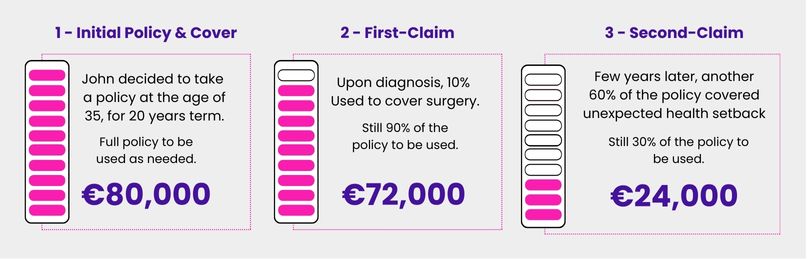

How is Multi Claim Protection Cover amount determined on severity?

Claim Events for MCPC

Multi-Claim Protection Cover allows more than one claim and continues after a payout, as long as the full amount of cover has not been used. This reflects the significant advances in medical diagnosis and treatment, which mean people are increasingly living longer and recovering from serious illnesses.

As a result, more people are being diagnosed earlier and successfully treated for serious conditions. This also means that some illnesses may have a less severe long-term impact than they once did, which is why Multi Claim Protection assesses claims based on severity rather than a one-time diagnosis.

For example, 1 in 2 people in Ireland will develop cancer during their lifetime. Thanks to earlier detection and improved treatments, many people recover or manage their condition and continue with their lives. Multi-Claim Protection Cover recognises this reality by allowing for partial claims and ongoing cover, where appropriate.

Cost example

As an example, a single, non-smoker aged 39, looking for €100,000 of Multi Claim Protection Cover over a 25-year term, could expect to pay approximately €45.77 per month. Actual premiums will depend on age, health, smoking status, and the level of cover chosen.

If you would like a personalised quote or a comparison of providers, our advisors can guide you through the options and help you find the right level of protection.

What is helping hand benefit?

Royal London’s Helping Hand benefit provides one-to-one personal support for you and your family during difficult times, at no extra cost. It is available as part of eligible Royal London protection policies and is designed to support both your physical and emotional wellbeing.

Helping Hand gives you access to a dedicated team of medical and wellbeing experts who can support you before, during, and after a serious illness diagnosis.

This free benefit includes access to:

Bereavement counsellors, speech therapists, physiotherapists, massage therapists, and face-to-face medical opinions for serious health conditions

Cardiac rehabilitation support

Specialist support for coping with cancer, including emotional and practical guidance

Family support services, including help following the loss of a loved one

Helping Hand is available even if you never make a claim, and support can be extended to your immediate family members, depending on the service. This makes it a valuable wellbeing benefit, not just a claims-related service.

You can learn more about Royal London’s Helping Hand benefit.

If you would like to understand how this benefit works alongside your protection cover, our advisors can explain what is included and help you choose the right policy for your needs.

Main Differences between MCPC and Health Insurance.

It is important to note that Multi-Claim Protection Cover and Health Insurance can work alongside each other, rather than replacing one another. Each serves a different purpose, and together they can provide more comprehensive financial and medical support.

Multi-Claim Protection Cover focuses on providing tax-free cash payments if you experience a serious illness or health setback, based on the severity of the condition. These payments are designed to help cover everyday expenses such as mortgage repayments, household bills, or loss of income during recovery.

Health Insurance, on the other hand, primarily covers medical treatment costs, such as hospital stays, consultant fees, and access to private healthcare services. It does not usually provide a direct cash payout to the policyholder.

In summary:

What does it pay out for?

Multi-Claim Protection Cover pays a cash benefit for serious illnesses or health events, based on severity. Health Insurance pays for medical treatment and hospital care.

Who does it pay out to?

Multi-Claim Protection Cover pays directly to you. Health Insurance pays hospitals or medical providers.

Can it pay out multiple times?

Multi-Claim Protection Cover can pay out more than once, provided the full cover amount has not been used. Health Insurance does not provide cash payouts.

How are payments used?

Multi Claim Protection Cover pays a guaranteed, tax-free percentage of your total cover, which you can use however you need. Health Insurance does not provide cash payments for living expenses.

Does it provide a financial payout on death?

Multi-Claim Protection Cover can include a death benefit, depending on the policy. Health Insurance does not provide a death benefit.

For a detailed comparison between Multi-Claim Protection Cover and Health Insurance, you can view Royal London’s guide.

If you are unsure which type of cover is right for you, or how they can complement each other, our advisors can explain the differences and help you choose the most suitable protection for your circumstances.