If you’re living with your partner but aren’t married, you may not realise the impact inheritance tax could have on life insurance payouts. Unlike married couples, cohabiting couples in Ireland are treated differently when it comes to taxes, meaning a significant portion of your inheritance could be lost to the taxman.

Luckily, there are ways to protect your loved ones from hefty tax bills and ensure that the full value of your life insurance payout reaches your partner. In this article, we’ll walk you through the options available to cohabiting couples, so you can make informed decisions to safeguard your financial future.

What Is A Cohabitation Relationship?

Cohabitation is when two people live together in a committed relationship without being married or in a civil partnership. This can include both opposite-sex and same-sex couples. Even though they’re not married, cohabiting couples can still share a deep connection, whether or not their relationship is romantic or sexual.

Although cohabiting couples do have some rights if the relationship ends or one partner passes away, they don’t have the same legal protections as married couples or civil partners. This can affect important things like owning property, raising kids, and what happens to your inheritance.

What is Inheritance Tax?

Inheritance tax, or Capital Acquisitions Tax (CAT), is a tax you pay on anything you inherit when someone passes away. This could include things like money, property, pensions, or even personal items.

The amount of tax you owe depends on the total value of everything you inherit.

You’re allowed to receive gifts and inheritances up to a certain limit during your lifetime before you have to start paying this tax.

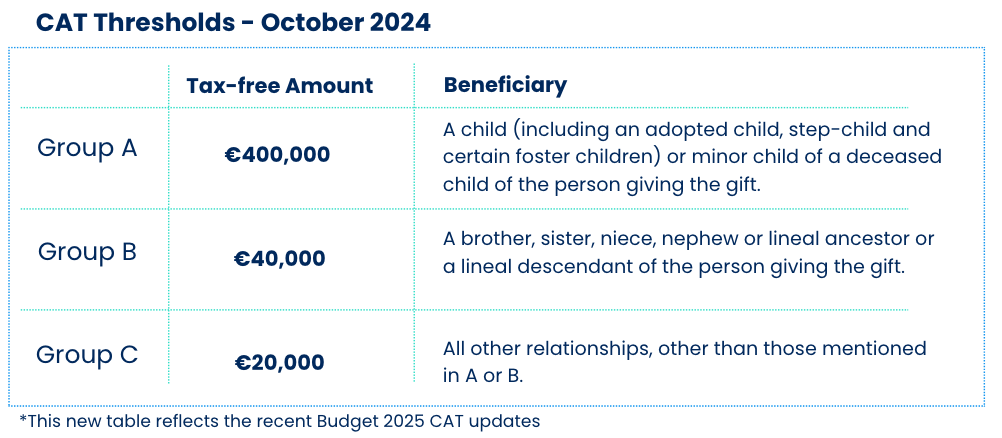

CAT – Group Thresholds

The amount of Capital Acquisitions Tax (CAT) you need to pay is based on your relationship with the person giving you the inheritance or gift. There are three different groups that determine this.