Many self-employed people in Ireland are unaware of the wide range of tax reliefs and strategies available to them. Whether you’re a sole trader or running a limited company, there are plenty of legitimate ways to reduce your tax liability and hold on to more of your hard-earned income.

With the right planning, especially if you own a business, you can make your money work smarter and more efficiently.

Here are some of the most effective tax-saving strategies for the self-employed in Ireland.

Contribute to a Pension and Cut Your Tax Bill

If you’re self-employed, contributing to a pension is one of the most effective and tax-efficient ways to reduce your income tax bill. The government offers tax relief as an incentive to help you save for your future.

Here’s how it works:

When you contribute to a personal pension or Personal Retirement Savings Account (PRSA), you can claim tax relief at your marginal rate, that’s either 20% or 40%, depending on how much you earn.

This means that for every €100 you contribute, the actual cost to you could be as little as €60 if you’re on the higher tax rate, with the remaining €40 effectively covered through tax savings.

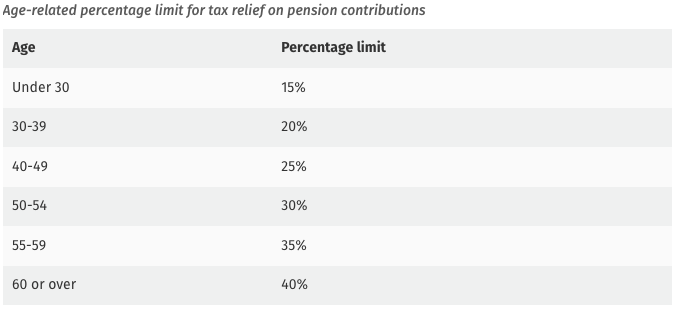

How much can you contribute?

It depends on your age. The older you are, the higher the percentage of your income you can put into your pension and still get tax relief:

No matter how much you earn, you can only claim tax relief on income up to €115,000. So even if you earn €200,000, the maximum amount that qualifies for tax relief will be based on €115,000.

Boost Your Pension Funds with AVCs

Making Additional Voluntary Contributions (AVCs) is a smart way to increase your pension savings while reducing your income tax bill.

If you’re already part of an occupational pension scheme or have a PRSA, AVCs let you top up your pension fund with extra contributions on top of your regular payments. These extra contributions qualify for tax relief at your marginal rate—20% or 40%—making them especially valuable for higher earners.

In simple terms, you’re not only boosting your retirement pot but also paying less tax today. AVCs are a flexible and effective way to take control of your long-term financial future.