What happens to my pension when I leave a company?

When you leave a job, what happens to your pension depends on the type of pension scheme you have and the conditions of that specific scheme. The three main options are

- Leave the Pension where it is: In some cases, you may have the option to leave your pension funds in the scheme, allowing them to continue growing until your selected retirement age.

- Transfer to a new employer’s scheme: If the job you’re moving to offers a pension scheme, you might have the option to transfer your pension savings to the pension plan of your new employer.

- Transfer into a Personal Retirement Bond (PRB).

It’s important to review the specific terms and conditions of your pension scheme or you can contact LowQuotes for personalised guidance on the best course of action based on your individual circumstances.

How do I choose a pension provider in Ireland?

When choosing a private pension provider in Ireland, it is important to consider factors such as personal circumstances, work situation, fees, investment options, and the provider’s track record.

At LowQuotes, our advisors can guide you through the process of choosing the best provider that meets your needs and help you make an informed decision.

Can I put a lump sum into a pension?

Yes, you can top up your pension with a lump sum as well as with regular contributions with Additional Voluntary Contributions (AVC).

This option is available for both a personal pension and a PRSA (Personal Retirement Savings Account).

The benefits of making AVC are:

- Top up your pension at any time so that you receive a larger pension upon retirement.

- You may be able to retire earlier with the help of an AVC by filling in the gaps in your pension payments.

- Avail of tax relief on investments depending on your marginal rate of tax.

- Choose to make contributions to your pension through your company or privately.

- You can increase, decrease, pause, or restart your AVC contributions at any time.

- Tax-free investment growth.

Can I increase my pension contributions?

Yes, you can usually increase your pension contribution whether you have a personal pension, an occupational pension, or a PRSA (Personal Retirement Savings Account).

You can make Additional Voluntary Contributions – AVC to increase retirement savings, maximise tax relief, potentially boost your pension fund’s growth over time, and enable you to retire early.

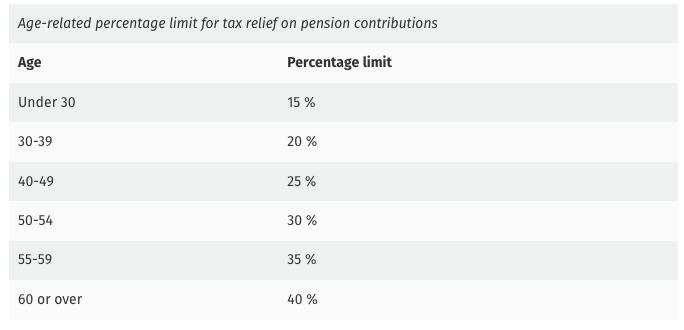

Is there a limit to how much of my earnings I can contribute and for which I can claim tax relief?

Yes. There are age-related contribution limits for pension contributions made by individuals, regardless of whether they are employees of companies or self-employed.

For example, an employee who is aged 42 and earns €40,000 can get tax relief on annual pension contributions up to €10,000.

The maximum annual earnings taken into account for calculating tax relief is €115,000.

1 thought on “The Essential Guide to Pension and Retirement Planning”

Comments are closed.