Table of Contents

Once upon a time in Ireland, you got married and bought your first home in your 20s. By the time you reached your late 50s, the mortgage was paid off, and you could enjoy retirement without money worries. The path to owning a home has changed a lot in recent years.

According to the Central Statistics Office, the median age of home purchasers in Ireland reached 40 in 2024, up from 35 in 2010. This is the most up-to-date official figure and reflects a clear generational shift. High property prices, the cost of living, and the time needed to build a deposit mean that more people are buying their first home later in life, often well into their 40s.

Are People Buying Homes Later in Life?

Yes, and the trend is firmly established. The latest CSO data (covering 2022 to 2024) shows that the median age of all home purchasers stood at 40 for three consecutive years, while almost a third of buyers in 2024 were aged 35 or under and around 11% were aged 60 or over.

By Type of Buyer:

- Sole purchaser with children: 43 years

- Sole purchaser without children: 42 years

- Joint purchasers with children: 40 years

- Joint purchasers without children: 36 years

The gap between sole and joint purchasers is significant. A single person buying a home in Ireland is typically four to five years older than a couple buying together, reflecting how much longer it takes to save a deposit on one income.

Regional Picture

Age also varies sharply by location. In 2024, the youngest buyers were in South Dublin with a median age of 37, while the oldest were in Kerry at 45. Urban local electoral areas such as Ballyfermot-Drimnagh in Dublin City had a median age of 35, while rural areas like Belmullet in Mayo sat at 54. Where you are buying can affect not just the price you pay, but the age profile of the people around you competing for the same homes.

What Has Changed Since 2010

The shift has been dramatic. In 2010, the median buyer was 35 years old. By 2024, that had risen to 40, a five-year jump in just over a decade. For sole purchasers, the change is even more pronounced. On top of this, the median income of home buyers has risen to €84,400 in 2024, up from €75,600 in 2022, showing that buyers are not only older but also need to earn significantly more to get onto the property ladder.

Your Future Home Could Be Closer Than You Think – Get a Quote Today.

What’s Pushing Buyers to Wait?

More and more people are delaying homeownership due to factors like:

High Property Prices

House prices in Ireland have risen significantly over the last 20 years. This makes it harder for younger people to afford a home, especially if they’re on one income or just starting their careers. In 2025, house prices continued to climb. According to the CSO Residential Property Price Index, households paid a median price of €387,000 for a dwelling in the 12 months to December 2025, with Dublin at €500,000 and Dún Laoghaire-Rathdown reaching nearly €680,000.

If soaring house prices have you thinking homeownership is out of reach, you’re not alone. But don’t give up just yet — our article has practical tips to help you budget for your home, even when prices are sky-high.

Later Marriage

In Ireland today, people are getting married later than ever, with the average age nearly 36 for women and 38 for men in 2024.

Between 2014 and 2024, people in Ireland started getting married later. In opposite-sex marriages, the average age of brides went up from 33 to nearly 36, and grooms from 35 to almost 38. Same-sex couples saw a small increase too, with women rising from 39.3 to 39.7 and men from 39.8 to 40.7 between 2019 and 2024. This shows a clear trend — people are waiting longer to get married, and that often means waiting longer to buy a home too.

Starting Families Later

The average age of first-time mothers reached 31.7 years in 2024, up from 30.5 in 2014, and 28.5 back in 2004. That’s an increase of over three years in just two decades. Many couples choose to rent while they focus on careers or save money, only deciding to buy a home when they’re ready to start a family.

Others may wait until after their children are born to look for a larger home that better suits their needs. This shift in timing is another reason why homeownership is happening later in life.

Career Building Comes First

Another key reason people are buying homes later in life is that many are spending their 20s focused on building their careers.

According to the Central Statistics Office’s Growing Up in Ireland study, a large number of 25-year-olds still live with their parents — mostly for financial reasons. In fact, 62.4% said money was the main reason they hadn’t moved out, while only 12.4% said it wasn’t about finances. This trend is closely linked to staying in education longer and needing more time to establish a steady income before making big financial moves like buying a home.

Rising Cost of Living

The rising cost of everyday essentials — like rent, childcare, transport, and food — is making it harder for people to save for a mortgage deposit. With a significant portion of their income going towards monthly expenses, many find it challenging to save money, which delays their ability to buy a home.

If you’re in the same boat, check out our article with Tips for Saving Money Towards Your Mortgage Deposit to help you get started.

Relationship Changes and Separation

More people are buying homes later in life due to relationship changes like divorce or separation. Starting over financially after a breakup can be challenging, especially when it comes to saving for a deposit or qualifying for a mortgage on your own.

However, if you no longer have a share in a property, you may be eligible as a first-time buyer again. Rebuilding after a split isn’t easy, but our guide on Rebuilding Your Finances After Divorce can help you take the next steps with confidence.

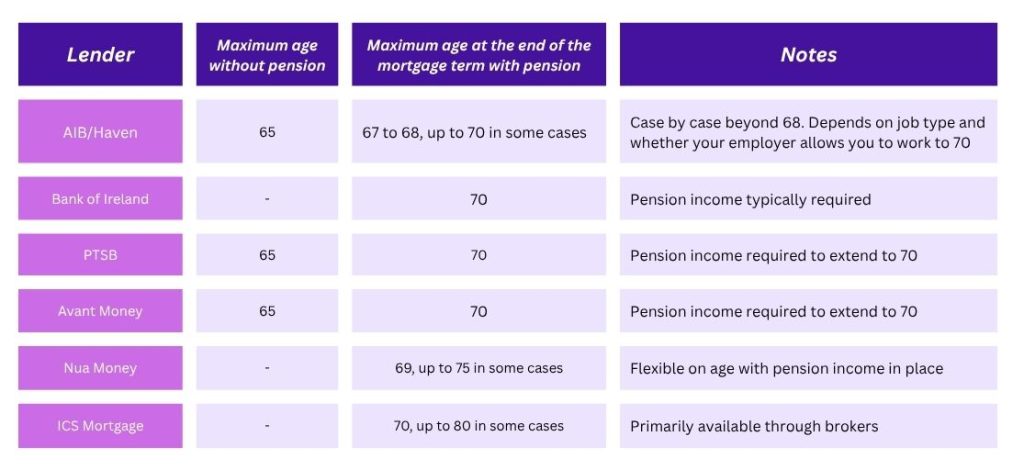

Is There an Age Limit for Getting a Mortgage?

Each lender in Ireland sets its own maximum age for mortgage repayment, not for application. The key factor is whether you have a pension in place, as most lenders will extend the age limit if you can show pension income to cover repayments past retirement. The table below reflects current lender criteria as of 2026. Always confirm directly with the lender or a mortgage advisor, as the criteria can change.

What this tells you: Your pension is often the single biggest factor in extending your mortgage term. If you are in your 40s or 50s and thinking about buying, starting or reviewing your pension now can directly improve your borrowing position later.

A mortgage broker can quickly tell you which lender will accept your age and income profile without impacting your credit score.

A mortgage broker can quickly tell you which lender will accept your age and income profile without impacting your credit score.

Real Scenario: Getting a Mortgage at 42 on a €70,000 Income

Meet Sarah, 42, a marketing manager earning €70,000 gross per year. She is single, has no dependants, and has saved a €50,000 deposit over eight years. She wants to buy a home priced at €320,000.

Here is how her application looks in practice:

- Maximum borrowing: Under Central Bank rules, a first-time buyer can generally borrow up to 4 times gross income, so €280,000.

- Deposit required: 10% for first-time buyers, so €32,000. Sarah has €50,000, which strengthens her case and can reduce the loan-to-value ratio.

- Mortgage term: Most lenders will take her to age 70, so she can get a term of up to 28 years.

- Monthly repayment: On a €270,000 mortgage over 28 years at a 3.9% rate, her repayments would be roughly €1,365 per month.

What this tells us: Being 42 does not stop Sarah from getting a mortgage. Her borrowing capacity is determined by income, deposit, and term. The only real age constraint here is that she cannot extend the term beyond 28 years, which slightly increases her monthly repayment compared to a 30- or 35-year term. Rates and rules are illustrative and change regularly. Get a personalised quote for accurate figures.

Can You Extend a Mortgage Past Retirement in Ireland?

Yes, in specific circumstances. Most lenders require the mortgage to be fully repaid by age 65 to 70, but some will consider allowing the term to continue beyond state retirement age if you can prove your ability to keep repaying.

To extend past retirement, lenders typically want to see:

- A pension fund with a projected income sufficient to cover repayments

- Evidence of an Approved Retirement Fund (ARF) or annuity in place

- Rental income, investment income, or a business that will continue generating cash

- Mortgage protection or life cover that runs to the end of the term

Tip: If you are close to retirement age, it is often smarter to apply now rather than wait. Lenders assess the end age of the loan, not just your current age, so every year you wait shortens the term you can access.

Pros of Getting a Mortgage Later in Life

- More financial stability – higher income, better credit history

- Larger deposit – often built up from years of saving or a previous property sale

- Stronger decision-making – clearer on life goals and where you want to live

- Pension-backed repayment options – some can use retirement income to qualify

- Homeownership into retirement means no rent to pay later in life

- Access to first-time buyer schemes – in certain cases, like post-divorce

The ultimate guide for First-Time Buyers.

Get instant access to a complete GUIDE that will save you the hassle and prepare you for a mortgage, providing a convenient checklist of essential documents and step-by-step instructions to help you secure your dream home. Don’t wait, download now!

Your homeownership journey starts here!

After you download your guide, one of our expert mortgage advisors will be in touch shortly to provide you with guidance and further relevant information including typical repayments, qualification amounts and mortgage requirements.

Cons of Getting a Mortgage Later in Life

- Shorter loan term – due to age limits on when the mortgage must be repaid

- Higher monthly repayments – shorter terms usually mean higher costs

- Stricter affordability checks – especially as you approach retirement

- Higher insurance premiums – age can raise the cost of life insurance or mortgage protection

- Less time to build equity – lower potential gains from future property value

- Possible impact on retirement plans – less flexibility to save or adjust if needed

(Fewer working years left to recover from setbacks like illness or job loss)

What’s the best age to be mortgage-free?

There’s no one-size-fits-all age when you should be mortgage-free — it really depends on your personal finances, goals, and retirement plans. However, we suggest aiming to have your mortgage paid off by the time you retire, typically between the ages of 65 and 70.

Here’s why:

- Fixed or lower income in retirement: Without a regular salary, paying off a mortgage can be more difficult.

- Peace of mind: Being mortgage-free means lower monthly expenses and more financial freedom in retirement.

- Pension protection: It helps preserve your retirement savings for living costs rather than loan repayments.

Some people do choose to keep a mortgage into retirement, especially if it’s small, affordable, and fits into their overall plan. They might be using their money in other smart ways, like investing or running a business. Ideally, it’s best to be mortgage-free by the time you retire, but if your repayments are manageable and you’ve planned well, it’s not a strict rule.

Key Things to Keep in Mind for a Mortgage Later in Life

Your Age Affects the Loan Term: Most lenders want the mortgage paid off by age 65 to 70, so the older you are, the shorter the loan term — and the higher the monthly repayments.

Retirement Income Matters: If you’re near or past retirement age, lenders may ask for proof of pension income or other financial support to make sure you can afford repayments long-term.

Affordability Checks May Be Stricter: Lenders often apply more caution when assessing borrowers later in life. They may look closely at your debts, dependents, and retirement plans.

You May Need a Bigger Deposit: A larger deposit can help you qualify more easily, especially if your income is lower or your term is shorter. It also reduces the loan amount and monthly payments.

Insurance Costs Could Be Higher: Mortgage protection and life cover may be more expensive as you get older. Be sure to factor this into your monthly budget.

Impact on Retirement Planning: A mortgage in your 50s or 60s might limit your ability to contribute to your pension or leave less financial flexibility in retirement.

You Might Qualify as a First-Time Buyer Again: If you’ve separated or sold a previous home and no longer have ownership, you may be eligible for first-time buyer supports like the Help-to-Buy scheme.

Get Professional Advice: A mortgage broker or financial advisor can help you find lenders that work with older buyers and tailor a plan to fit your stage in life.

FAQ - People also ask

No. Forty is now a very common age for first-time buyers in Ireland. The median age for a joint purchaser without children was 36 in 2021, and for sole purchasers, 41. Lenders care about your ability to repay between the ages of 65 and 70, not your current age.

Yes. Most lenders will offer a mortgage with a term of up to 20 years at age 50, assuming the loan ends by age 70. You will face a shorter term than a younger applicant, which increases the monthly repayment but does not prevent approval.

It is possible, but more restrictive. You will need strong evidence of retirement income, typically through a pension, ARF, or annuity. Some lenders allow terms of 5 to 10 years past age 65 if affordability is clear.

Most lenders set the maximum age at the end of the mortgage term at 70. A smaller number goes to 68. There is no maximum age to apply, only a maximum age by which the loan must be repaid.

Read Our Articles

If you’re thinking about stepping onto the property ladder, we’ve put together some must-read articles to help you get prepared. From saving for a deposit to getting a mortgage later in life, these guides are full of practical tips to make your journey smoother.

- Essential Steps for Getting Mortgage Ready

- Can a single person get a mortgage in Ireland?

- Home Sweet Home: The Ultimate First-Time Buyer’s Guide

- Hidden Extra Costs When Buying a House in Ireland

- Tips for Saving Money Towards Your Mortgage Deposit

- 10 First-Time Buyer Mistakes to Avoid in Ireland

- Mortgage Protection Insurance in Ireland: Everything You Need to Know

- How to Budget for a House When Prices Are Through the Roof

If you are unsure what is possible based on your age, we can quickly assess your options with no impact on your credit score.

Get a Mortgage Quote With LowQuotes

More and more people are buying homes later in life — and doing it successfully. Don’t let old ideas about the “right” age to buy hold you back. With smart planning and the right support, you can still achieve homeownership on your own terms. Start by getting a personalised mortgage quote with LowQuotes and take the first step toward your future home.

Whether you’re already working on your deposit, figuring out monthly repayments, or just want to understand your options, we’re here to help you prepare with confidence. Let’s make sure your finances are ready for this exciting step.

We provide various financial services, including life insurance, income protection, mortgages, serious illness cover, pensions, financial planning, health insurance, and savings & investments.

Share this post

All our content has been written or overseen by a qualified financial advisor. However, you should always seek individual financial advice for your unique circumstances.