ARF vs Annuity – A quick comparison

When people retire, they often compare an ARF with an annuity, because both are options for using their pension fund.

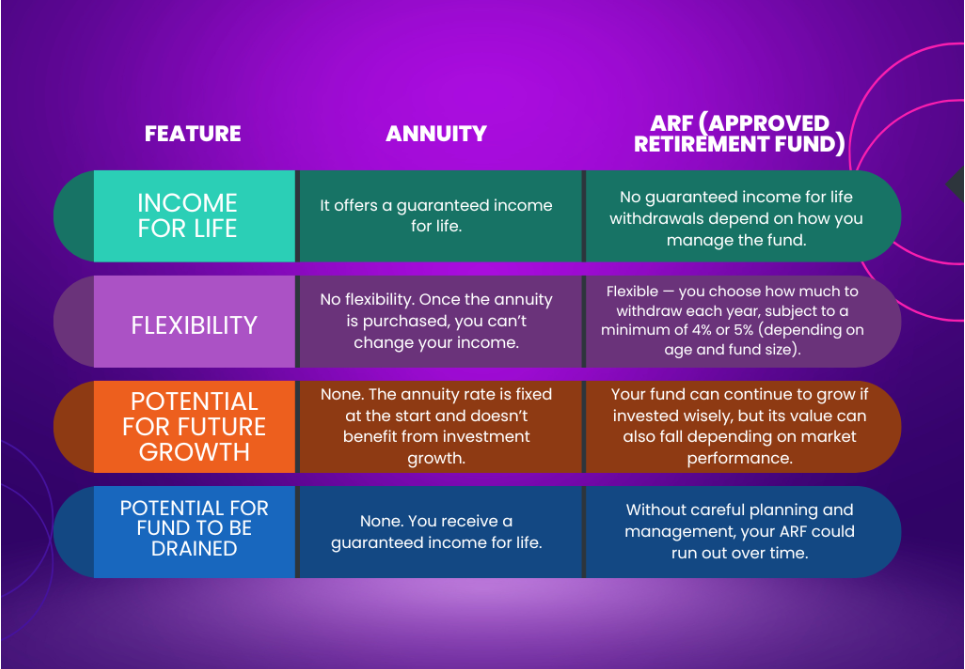

An annuity gives you a guaranteed income for life. Once you buy it, your money is handed over to an insurance company, which pays you a fixed amount every month or year. It’s predictable and low-risk, but there’s little flexibility. If you pass away earlier than expected, your income usually stops or continues only for a short period, depending on your policy.

An ARF, on the other hand, keeps you in control of your pension fund. Your money remains invested, and you can draw it down as needed. This means you have flexibility, growth potential, and the ability to leave the remaining balance to your loved ones. However, it also means you take on the investment risk, your fund could go down in value, and there’s no guarantee it will last for your entire retirement.

In short, if you prefer stability and certainty, an annuity might suit you. If you value flexibility and are comfortable managing some investment risk (with advice), an ARF could be the better fit.

Note:

Once an ARF policyholder turns 61, a minimum annual withdrawal of 4% of the fund is required.

This increases to 5% per year once they reach 71 years old.

If the ARF value exceeds €2,000,000, the minimum annual withdrawal rises to 6%.

Is an ARF right for you?

Before deciding, ask yourself a few questions:

- Do I want flexibility in how I access my retirement money?

- Am I comfortable with investment risk?

- Is leaving money to my family important to me?

- Do I have other income sources, like the State Pension?

If you said yes to most of those, an ARF might be a good match. But as always, it’s best to discuss your personal situation with a qualified financial advisor, someone who can help you understand the tax rules, investment options, and long-term sustainability of your withdrawals.

Looking for More Guidance?

We’ve created The Essential Guide to Pension and Retirement Planning, a clear, easy-to-follow resource that walks you through everything from building your pension to managing your income in retirement.

We also have two helpful articles if you’re nearing retirement:

Alternatively, you can always speak with one of our financial advisors.

They’ll help you understand your options, compare what’s best for your situation, and build a plan that fits your retirement goals. Whether you’re five years away or already retired, having expert guidance can make all the difference.