8. Online gambling

Having transactions on gambling websites doesn’t mean it will exclude you from being eligible for a mortgage. However, if there is a consistent history of transactions to betting sites this might raise a red flag with mortgage lenders. If you’re serious about saving for a house, cut out the betting.

9. Credit History

Lenders may be concerned if they see old arrears on a borrower’s credit history, even if they have been paid off. Late or missed payments, even if they occurred in the past, can have a negative impact on your credit score.

Even though having previous arrears on your credit report can be difficult, it doesn’t necessarily imply that you won’t be able to get a mortgage. Talk to one of our financial advisors to get personalised advice when it comes to mortgages. We can help you navigate the complexities of the mortgage process and find the best solution for your individual needs.

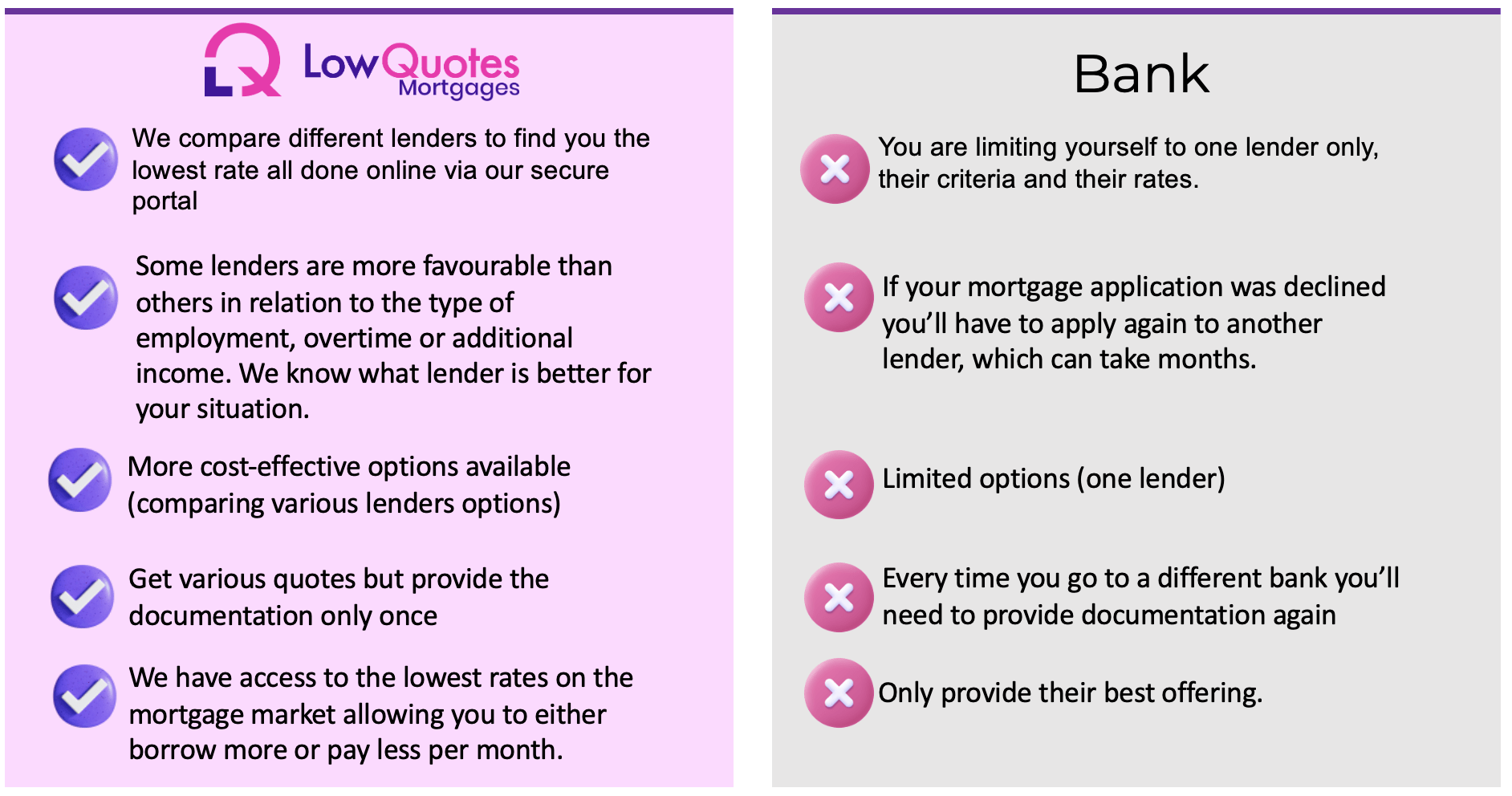

10. Stick with your bank

If you’re buying a home for the first time, going to the bank can seem like an obvious choice. However, this is a mistake because your bank might not be offering the cheapest or most suitable mortgage for your needs.

With a bank, you are limiting yourself to one lender only, their criteria, and their rates. While with LowQuotes we compare different lenders to find you the lowest rate.

Some lenders are more favourable than others in relation to the type of employment, overtime, or additional income. We know what lender is better for your situation and you can get various quotes from different mortgage providers.

On the other hand, with a bank, if your mortgage application was declined you’ll have to apply again to another lender, which can take months. Every time you go to a different bank you’ll need to provide documentation again.

This doesn’t happen with LowQuotes as we have your supporting documents submitted to our online system and can apply to additional lenders if one rejects your application.

Get your mortgage with LowQuotes

LowQuotes is your first stop when looking for the best mortgage offers. We ensure that you get access to competitive rates tailored to your specific needs. Whether you’re a first-time homebuyer or looking to switch or remortgage, our financial advisors are dedicated to guiding you through the mortgage process, making it seamless and stress-free.

Don’t miss out on the opportunity to secure your dream home with the help of LowQuotes. Start your journey towards homeownership today and experience the convenience of finding your perfect mortgage match in just a few clicks.