Wouldn’t it be wonderful if we could foresee the future and take action before things occur? If we had a heads-up about what’s coming next, we could get ready for potential risks or take advantage of positive outcomes.

Unfortunately, time machines are still science fiction, and we must be prepared for challenging situations that may arise in life.

If you identify the ‘what ifs’ that would have negative impacts on your life, it’s easier to put some financial protection in place to help your family if something happens to you.

This article aims to make you think about critical scenarios you may not have previously considered or, if you have, may be putting off for a number of reasons.

1. What if you got seriously ill?

Serious illnesses can strike unexpectedly, regardless of age, gender, or background. Whether it be cancer or heart disease, health issues can drastically change the course of your life.

They often come with substantial medical expenses, loss of income due to the inability to work, and many unforeseen costs. And this may impact your finances significantly.

To provide some financial protection if you suffer serious medical issues or illness, you can get a type of insurance called Serious Illness Cover, also known as Critical Illness Cover, which pays a lump sum if you’re diagnosed with a life-threatening illness that is covered and defined under the policy conditions. Examples would include some types of cancer, heart attack, or stroke.

Serious illness can help maintain your family’s standard of living or adapt your house for your illness, for example.

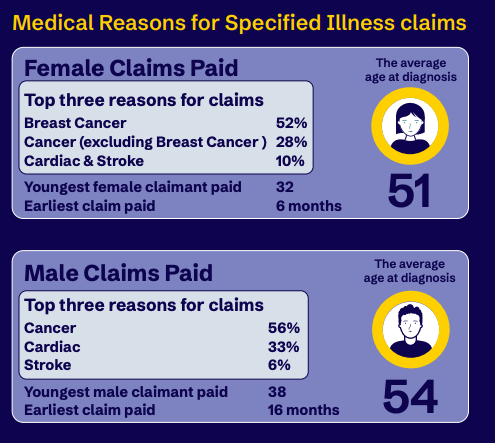

According to Aviva’s Report 2023, the most common medical reasons for specified Illness claims were breast cancer, cancer (excluding breast cancer), cardiac, and stroke.

Visit our post with the most frequently asked questions regarding serious illness cover if you want more information to help you decide.

Read our article 6 Things To Know Before Purchasing Serious Illness Cover to make informed decisions.

3. What if you weren’t around anymore?

The truth is, nobody likes talking about this topic, but death is the only certainty in life. The question you should ask yourself is: Would your loved ones be able to pay their living expenses when you’re not around anymore?

It’s important to have a plan in place to safeguard your loved ones in the event of your premature death. Life insurance pays out a lump sum if you die during the term of your policy. Your beneficiaries can use the payout from the life insurance company to cover various expenses, such as funeral costs, mortgage repayments, daily expenses, or the education of your children.

We put together some of the most frequently asked questions about life insurance to help you understand the basics of it, whether you’re thinking about purchasing a policy or are simply trying to understand your existing coverage.

There are many false beliefs about life insurance in Ireland that eventually discourage people from considering it as a viable alternative. Read our article about myths and misconceptions about life insurance.

Also, consider getting Convertible Life Insurance where you can extend your current policy without having to undergo a medical exam or show proof of good health at the time of conversion.