What is a specified serious illness cover in Ireland?

Specified serious illness cover in Ireland is a type of insurance policy that provides a lump sum payment that enables you to take care of yourself and your family if you are diagnosed with a life-threatening illness that is covered and defined under the policy conditions, examples would include some cancers, heart attack, or stroke.

This money can be used to cover things such as medical expenses or household bills. The illnesses covered and the amount paid out will vary depending on the policy and the insurance providers. We compare the prices of all providers in Ireland, and with the highest discounts available, you simply can’t get a better deal elsewhere.

Buying a standalone specified serious illness or adding accelerated serious illness to your life protection cover

You can buy serious illness cover as an extra benefit on a life insurance or mortgage protection policy. Or you can buy serious illness as a separate policy.

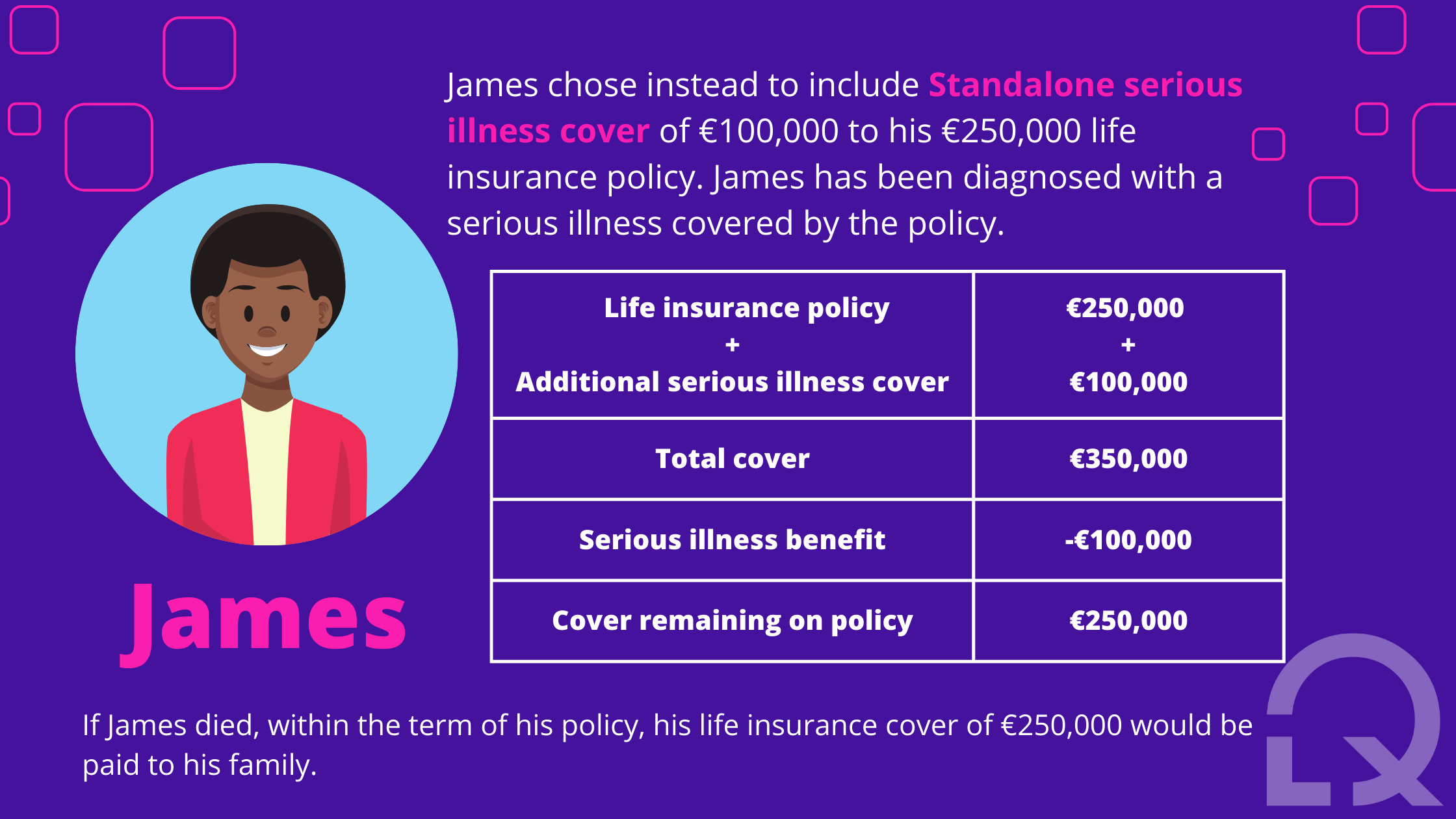

- Standalone serious illness cover means it is taken out as a separate policy and it is completely independent of any life protection you might purchase or already have. It is also sometimes called additional cover, separate cover, or double cover.

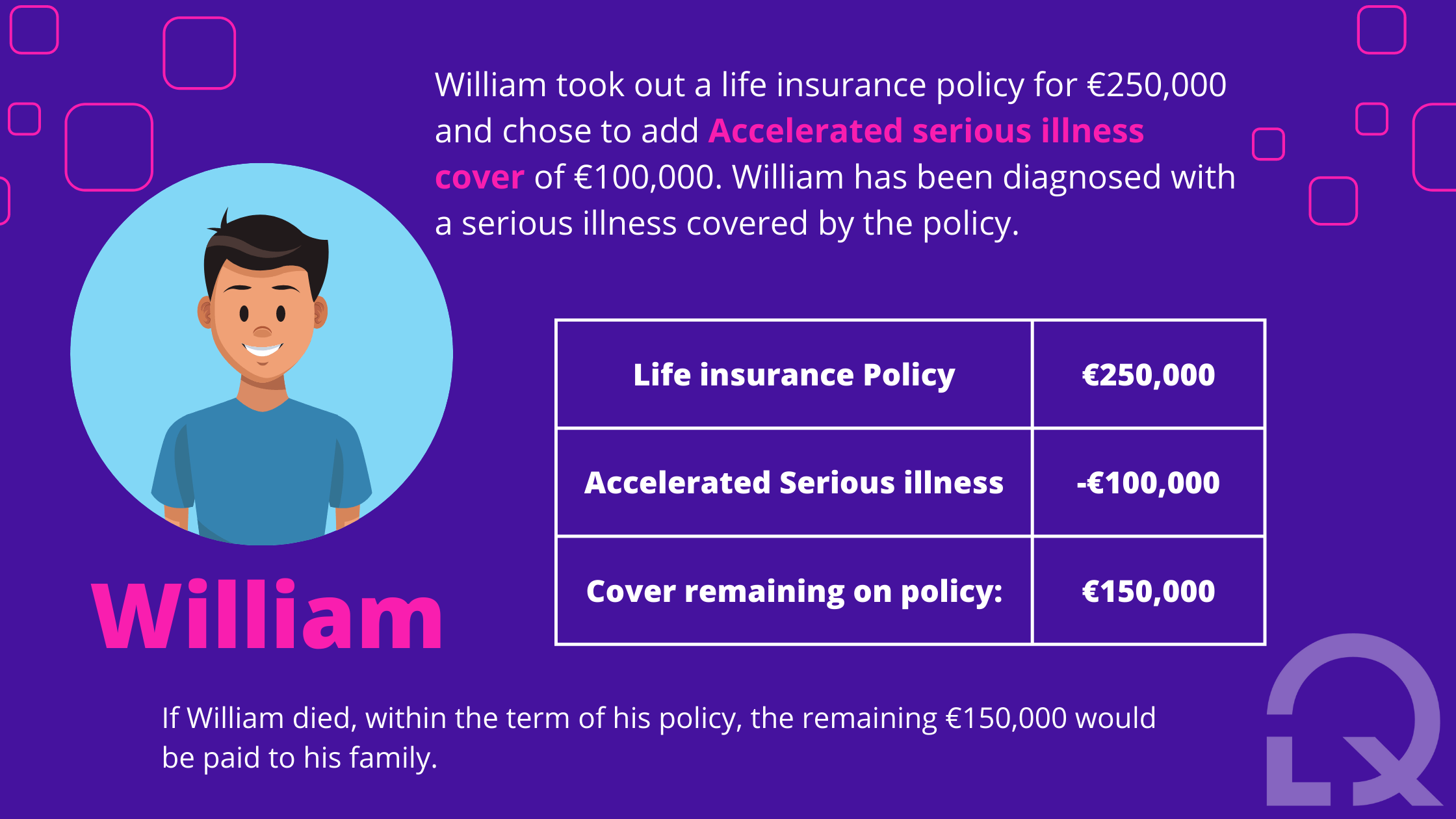

- If you are adding serious illness cover to your mortgage protection or life insurance when the payment is made the life cover amount is reduced accordingly. It is also called an accelerated serious illness cover.

How much does specified serious illness cover cost?

The price of specified serious illness in Ireland can vary depending on a number of variables, including the individual’s age, health condition, the desired level of coverage, and the kind of policy.

Keep in mind that there are many different types of specified serious illness insurance policies available.

Standalone Serious Illness: Serious illness cover only.

Life Insurance with Accelerated Serious Illness: your life insurance would be reduced by any amount paid under Accelerated Specified Illness Benefit.

Life insurance with Standalone Serious Illness: your life insurance stays the same regardless of any amount paid under Specified Illness cover. This cover is more expensive than the accelerated cover.

The best way to determine the cost of specified serious illness cover in Ireland is to speak with LowQuotes. We can help you understand your options and find a policy that is right for you and your budget.

Once accepted, the cost of your cover will never increase during the term of your plan, that’s why it’s important to purchase a serious illness policy as soon as possible when it is cheapest.

Age: 25 years old

Male – Non-smoker

Term: 30 years

Life Insurance cover: €250,000

Serious Illness cover: €100,000

Date of the quote: January 2025

Average Premium | |

Standalone Serious Illness | €30.98 |

Life Insurance + Accelerated Serious Illness | €35.90 |

Life Insurance + Standalone Serious Illness | €42.01 |

What percentage of specified serious illness claims are for cancer in Ireland?

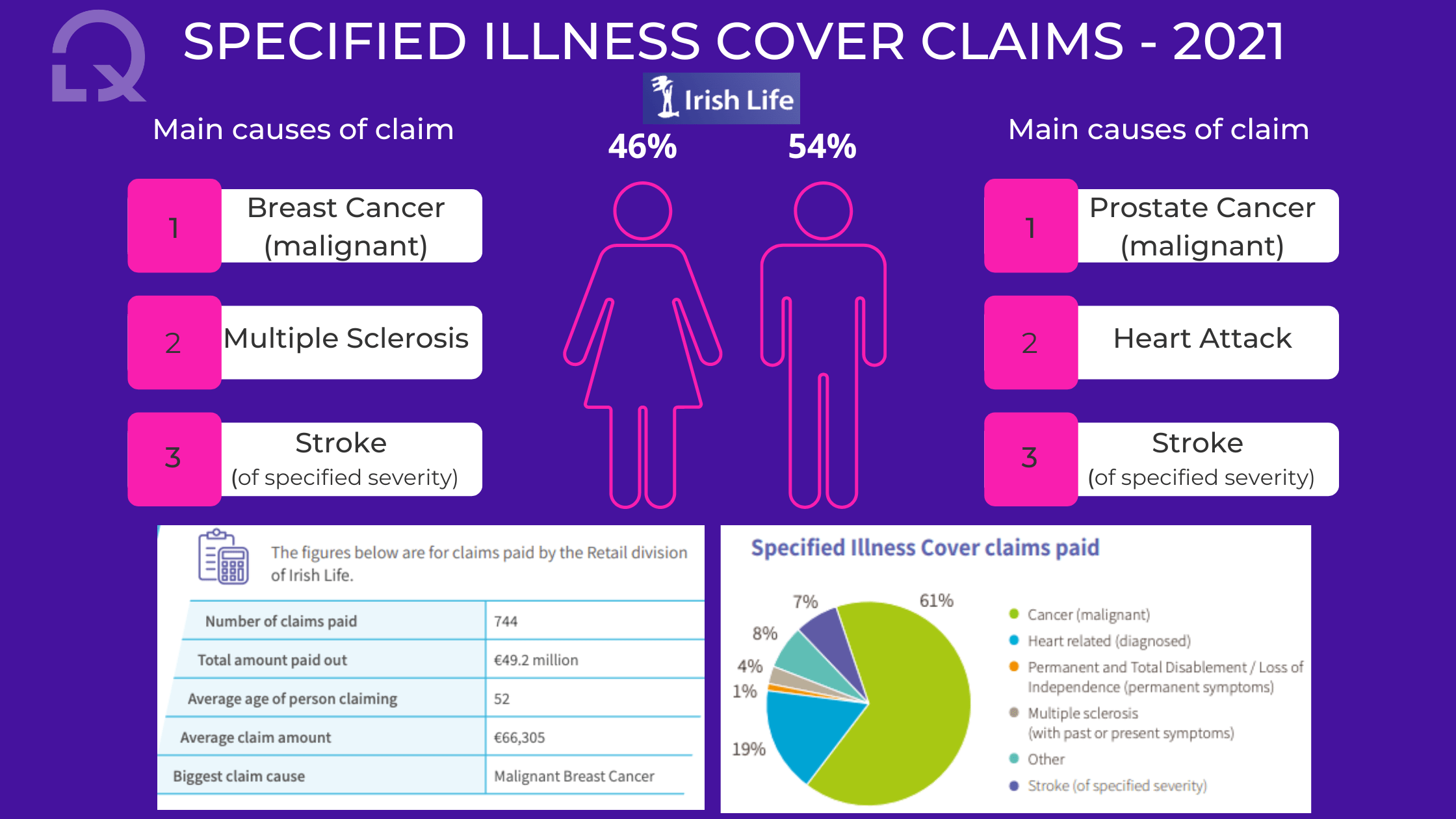

Back in 2018 according to Irish Life’s annual report, the main cause of Life Insurance pay-outs in 2018 was Cancer. Unfortunately, this scenario hasn’t changed and cancer is still the main reason for specified serious illness claims in 2021.

As stated by Irish Life, 61% of the specified Illness Cover claims paid was Cancer. The main cause for men was Prostate Cancer (54%) and Breast Cancer for women (46%).

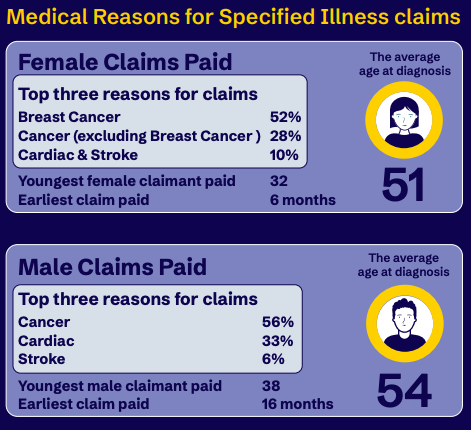

According to the Aviva report 2023, cancer is the main cause of claims for serious illness cover. The average age of claims is 54 for men and 51 for women.