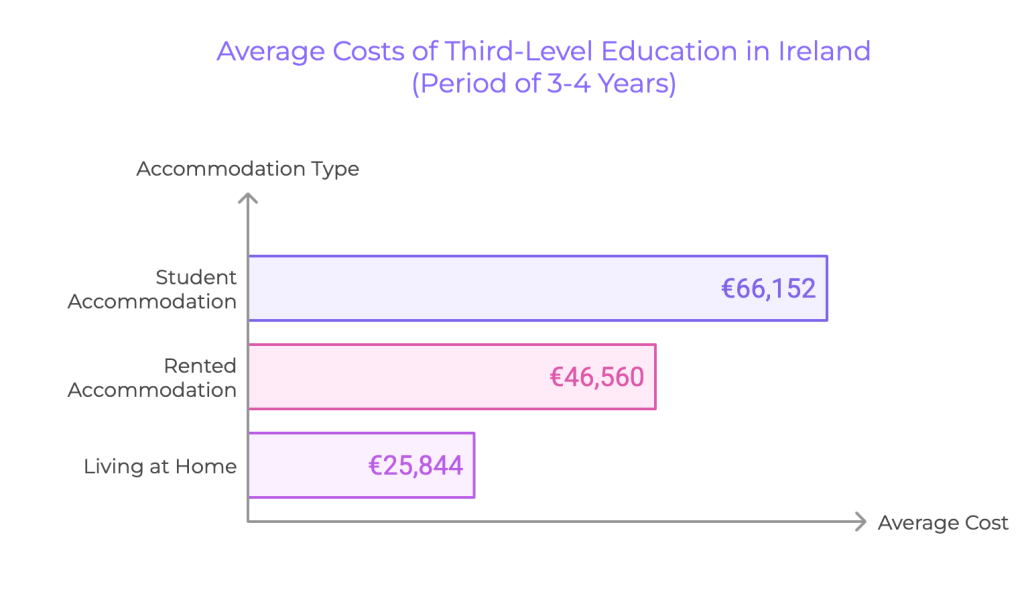

Differences between a regular savings account vs a children’s investment fund

Children’s investment fund is an account created with the objective of making investments for children. The account’s purpose in this case is to give the child long-term financial benefits, like a college fund or a future savings account.

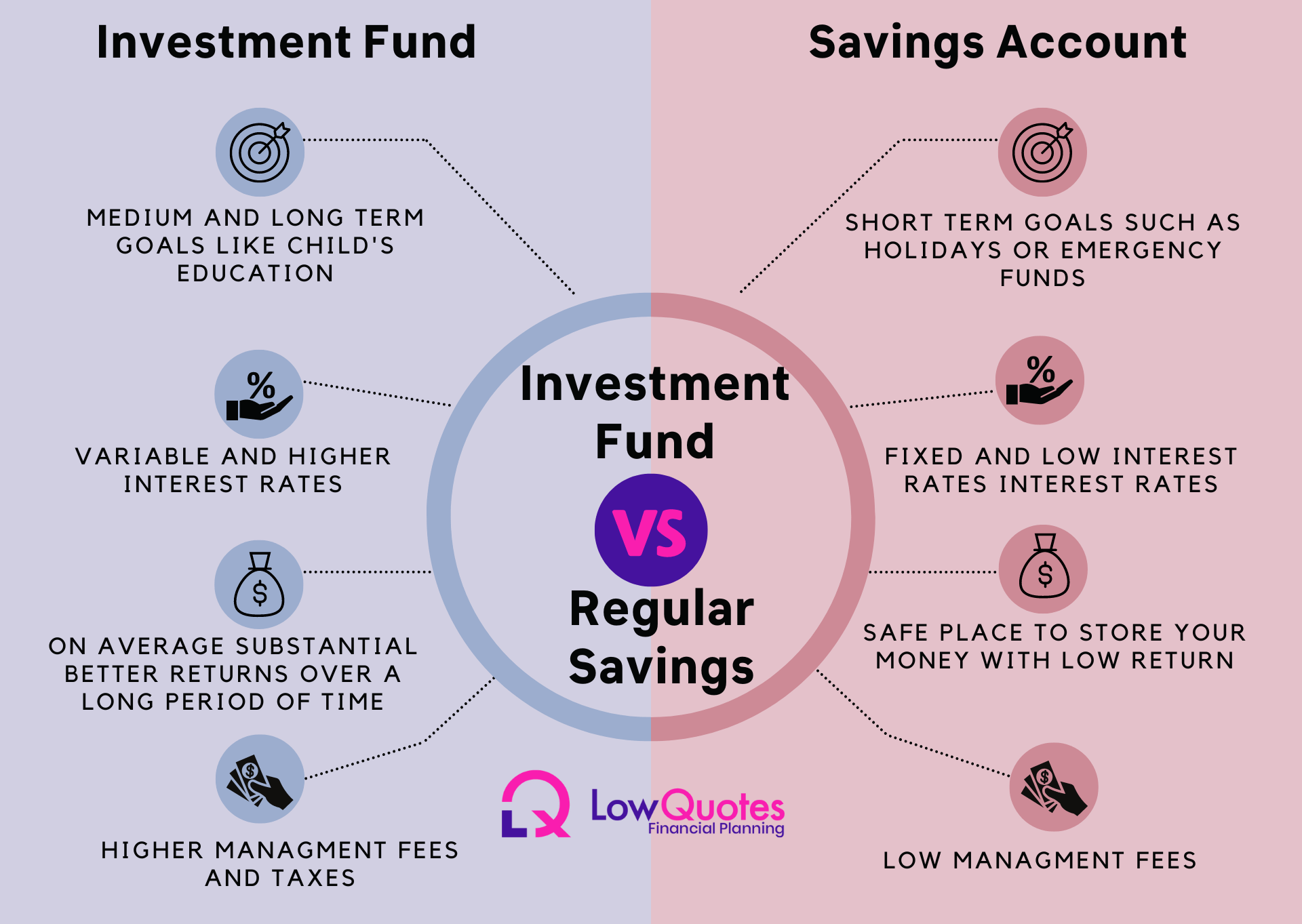

Your goals should be considered when choosing between a regular savings account and an investment fund. A savings account is only a good choice if you’re seeking a safe location to save your money for short-term goals, such as an emergency fund. An investment fund, on the other hand, can be a better option if you’re hoping to grow your money over the long term for events such as saving for your child’s education.

When choosing the best option between a savings account and an investment fund you need to consider your financial goals, level of risk tolerance, and time frame you want to reach your goal. Remember: to boost your savings, you don’t have to be rich or skilled. All you need to do is get advice from a qualified financial advisor. At LowQuotes we have a highly qualified team of financial advisors that can assist you with this, we will advise and help you to make a decision as to what is the best way to save for your child’s college.

We can help you make the right decision about saving for your child’s education as well as providing financial planning advice considering every aspect of your finances and creating a plan to meet your personal and financial goals.

How can a unit-linked fund help you save for your child’s education?

In a unit-linked savings plan, investors purchase units that correspond to a share of the fund’s overall assets. You can choose from a variety of investment funds when you first purchase the policy, and your selection of funds is valid for the duration of the coverage.

Opening a unit-linked savings plan is very simple, you can vary your payments whenever you like and you can choose which provider life funds to invest in at the beginning of it. This plan also makes full use of annual gift tax exemption limits.

This investment is suitable for those who have a long-term horizon and happy to save for a period of 5 years or more. You’ll need to decide how much you want to put aside each month – it can be as little as €100.

Comparing interest rates banks vs unit-linked funds

Some of the banks in Ireland offer interest rates on savings accounts for children that fluctuate from 0.01% to 1.00%. Unit-linked savings’ interest rates can be up to 10% or even more depending on the plan. Over the long term, the returns on deposit accounts are unlikely to match the returns you may enjoy from investing in the funds.

- EBS – Pay 1% with a maximum balance of €5,000.

- AIB- Get an interest rate of 1% on the first €1,000. All amounts above €1000 will earn a lower rate of interest.

- Bank of Ireland – The Childsave account pays an interest rate of 0.75% up to €10,000.

- Unit-linked fund – Pays up to 10% or more depending on the risk of the selected plan.

3 thoughts on “What is the best way to save for your child’s college education?”

Comments are closed.