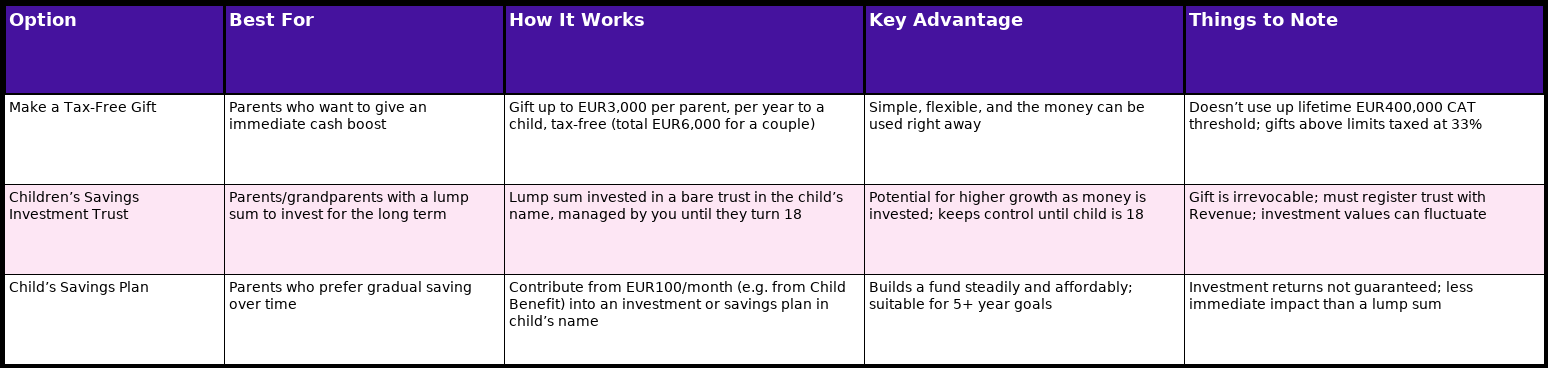

Children’s Savings Investment Trust

Let’s say you want to give your child a meaningful financial boost, whether for a future home, education, or just a solid foundation, but in a way that’s smart and tax-efficient. That’s where something like a Children’s Investment Trust comes in handy.

Here’s how it works:

- You invest a lump sum into an Investment Bond, which is held in what’s called a Bare Trust, essentially a long-term savings pot reserved just for your child.

- You stay in control as the trustee. This means you choose which funds to invest in, keep tabs on performance online, and make adjustments as needed.

- The trust locks everything in for the child until they turn 18, so the money can only be used towards something meaningful, such as a mortgage deposit, education, or a first car.

Why it’s a clever option:

- Growth potential: Unlike a regular savings account, your money gets invested in diverse funds and could grow substantially over time.

- Tax-smart: Contributions stay within the tax-free thresholds (like CAT limits), and any investment growth doesn’t count towards those thresholds. For example, if €40,000 grows to €83,000, the extra €43,000 isn’t taxed because only the original gift matters for tax purposes.

- Flexibility for the giver: You remain in charge as trustee, monitoring and adjusting investments until the funds are passed to the child at 18.

Things to keep in mind:

- Once the trust is set up, the gift is final—you can’t take the money back.

- It’s only for children under 18, and trusts must be registered with the Revenue for anti-money-laundering purposes.

If you’re looking to give your child a gift that grows, stays tax-efficient, and is carefully protected until they’re ready, a Children’s Investment Trust is a powerful way to set them up for real success, while giving you peace of mind that it’ll support them at just the right time.

Read more about Children’s Investment Trust.

Child’s Savings Plan

Another way to make steady progress towards your child’s financial future is with a Child’s Savings Plan, a solid and low-stress option.

Unlike a Children’s Savings Investment Trust, where you invest a lump sum upfront, a Child’s Savings Plan lets you contribute a small amount each month, starting from as little as €100, and gradually build a dedicated fund for your child over time.

Here’s why it works so well:

- Easy and reliable: Think of it like a regular savings account, but made specifically for your child’s future. It’s a smart, no-fuss way to start building a dedicated fund, especially for medium-term goals like college tuition or a mortgage deposit.

- Invest their Child Benefit payments wisely: In Ireland, you get €140 monthly in Child Benefit. Instead of letting it sit idle, consider putting it into a savings plan. Over time, that adds up, as it is parked in a fund and has room to grow.

- Long-term focus: This investment is suitable for individuals with a long-term horizon who are willing to save for a period of five years or more. You’ll need to decide how much you want to put aside each month – it can be as little as €100.

Read more:

The Key Takeaway on Gift & Inheritance Tax

All three of these options — the Small Gift Exemption, a Children’s Savings Investment Trust, and a Child’s Savings Plan — can be used without triggering gift tax, as long as you stay within the rules.

- €3,000 per parent, per year is always tax-free under the Small Gift Exemption. That means a couple can give a child up to €6,000 each year without paying any tax or filing paperwork.

- Over a lifetime, each child can receive a total of €400,000 from their parents (gifts and inheritance) before any Capital Acquisitions Tax (CAT) is due.

If you go above either the annual exemption or the lifetime limit, the excess is taxed at 33%.