What Kind of Pension Can You Set Up?

There are solid options available to self-employed workers in Ireland, with significant tax incentives to encourage you to start.

Personal Retirement Savings Account (PRSA)

A Personal Retirement Savings Account (PRSA) is a flexible and portable pension option, ideal for self-employed people with variable income. You can pause or adjust your contributions at any time to suit your financial situation, and the account stays with you if you change jobs or move abroad. Plus, contributions qualify for tax relief at your marginal rate—20% or 40%—making it a tax-efficient way to save for retirement.

Company Pension (via Limited Company)

If you’re self-employed and operate through a limited company, you can set up an Executive Pension or contribute to your own PRSA via your business.

Why it’s worth considering:

- Your company can make pension contributions on your behalf.

- These contributions are corporation tax-deductible.

- You can build a pension pot more quickly than by contributing personally.

Read more about how to grow your money transferring your company profits to your own pension funds: A Guide for Business Owners on Protecting, Extracting, and Growing Wealth in Ireland.

How Much Should You Contribute?

Figuring out how much to contribute to your pension starts with understanding how much you’ll need in retirement to maintain your lifestyle comfortably. While the exact figure will vary from person to person, a good rule of thumb is to save as much as you reasonably can, starting as early as possible.

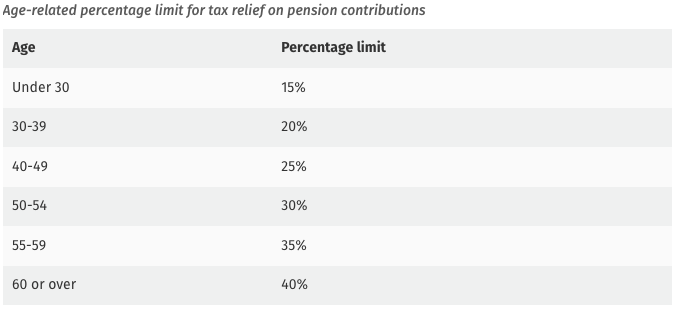

In Ireland, there are age-related limits on the percentage of your income that qualifies for pension tax relief, whether you’re self-employed or an employee. For example, if you’re 42, your contribution limit is 25% of your earnings. So, if you earn €40,000, you can contribute up to €10,000 per year to your pension and claim tax relief on the full amount.

The maximum annual earnings taken into account for calculating tax relief is €115,000.

When Can You Access Your Pension?

The age at which you can access your pension depends on the type of plan you have. If you set up a pension while self-employed or worked for an employer that didn’t contribute to your pension, you likely have a Personal Pension or PRSA.

In most cases, you can access your PRSA anytime between the ages of 60 and 75. However, in certain situations, such as if you retire early or stop working due to ill health, you may be able to start drawing benefits as early as age 50. Because each case is different, it’s always best to speak with a financial advisor to understand your specific options and timelines.

What Options Do You Have When You Retire?

When you retire, you’ve got a few solid options, and depending on your pension type, you might be able to combine them. The choices you have will depend on the kind of pension plan you’ve built up over the years, but in general, there are four main routes you can take.

- You can take 25% of your pension tax-free when you retire (up to a lifetime cap of €200,000).

- Take a taxable lump sum (any amount above the €200,000 limit is taxed).

The rest can be used to buy an annuity (guaranteed income for life) or go into an Approved Retirement Fund (ARF), which gives you more control and flexibility.

Read Our Articles

We’ve put together plenty of articles to guide you through key financial decisions. You might like the following:

- Why a Private Pension in Ireland Is Smarter Than You Think

- Setting Up a Private Pension in Ireland

- 6 Reasons to Review Your Pension This Year

- 7 Smart Ways to Use Tax Relief to Grow Your Pension in Ireland

- What to Do 5 Years Before Retirement

- The Essential Guide to Pension and Retirement Planning

- Private Pension Myths in Ireland

- Do You Know What Happens to Your Private Pension Plan When You Die?