How rising ECB Interest Rates can impact your mortgage repayments

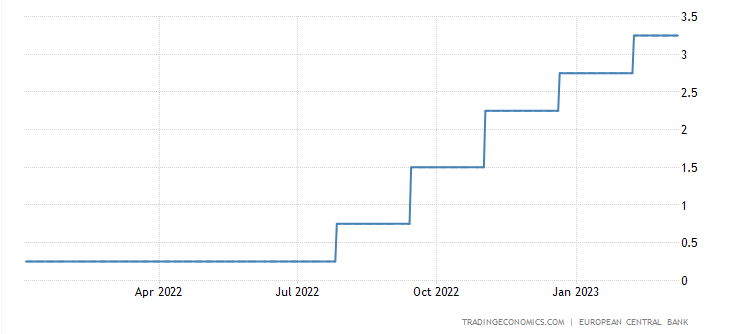

The most recent increase brought the deposit rate to 2.5% and the main lending rate to 3% in February 2023. Prior to that, in 2022, the ECB increased interest rates four times. And the Governing Council of the European Central Bank stated that it intends to raise interest rates by another 0.50% in March 2023 bringing the main lending rate to 3.5%.

The Central Bank of Ireland expects a recession and inflation for the Eurozone at 6.3% in 2023, which means there might be more interest rate increases to come.

ECB Interest Rates – April 2022 to February 2023

If you have a variable rate mortgage or a tracker mortgage, the ECB interest rates might have a major impact on your mortgage repayments. This is because the interest rate on these types of mortgages is usually linked to the ECB rate, which means that any changes in the ECB rate will be reflected in your mortgage rate. In other words, if the ECB raises its interest rates, your mortgage rate will also increase, which will lead to higher mortgage repayments.

If you have a fixed-rate mortgage, your mortgage repayments will not be affected by changes in the ECB rate during the fixed-rate period. However, when your fixed-rate period comes to the end your monthly repayments will increase. Lenders are required by law to tell you their cheaper options 60 days before your fixed-rate mortgage period ends.

However, they will only provide you with their best offer but this might not be the best deal available to you on the Irish market. That’s where we at LowQuotes can compare multiple lenders to guarantee you the cheapest rates.

Another situation is if your mortgage is a short-term fixed rate, you can break out of the fixed rate and lock into a long-term fixed rate in anticipation of the upcoming expected rate increases.

Remember that early termination of a fixed-rate mortgage may result in a penalty fee; however, in our experience, the cost of this fee should be weighed to any potential savings from changing your mortgage.

You must first check with your lender to determine whether there is a penalty before we can assess your situation and advise you on the best course of action for switching mortgages.

You should be aware of the impact of rising ECB rates on your mortgage repayments will depend on the size of your mortgage, the type of your mortgage, the interest rate on your mortgage, and the remaining term of your mortgage.

If you want to have an idea of what you could save by switching your mortgage each month, try out our Mortgage Switching Calculator or contact us, we will be happy to help you to give you the best advice on how to switch and save.

How much money can I save by switching my mortgage?

The amount of money you can save by switching your mortgage depends on a number of variables, including the current interest rates, the type of mortgage you have, the remaining duration of your mortgage, and any costs or potential penalties involved with moving.

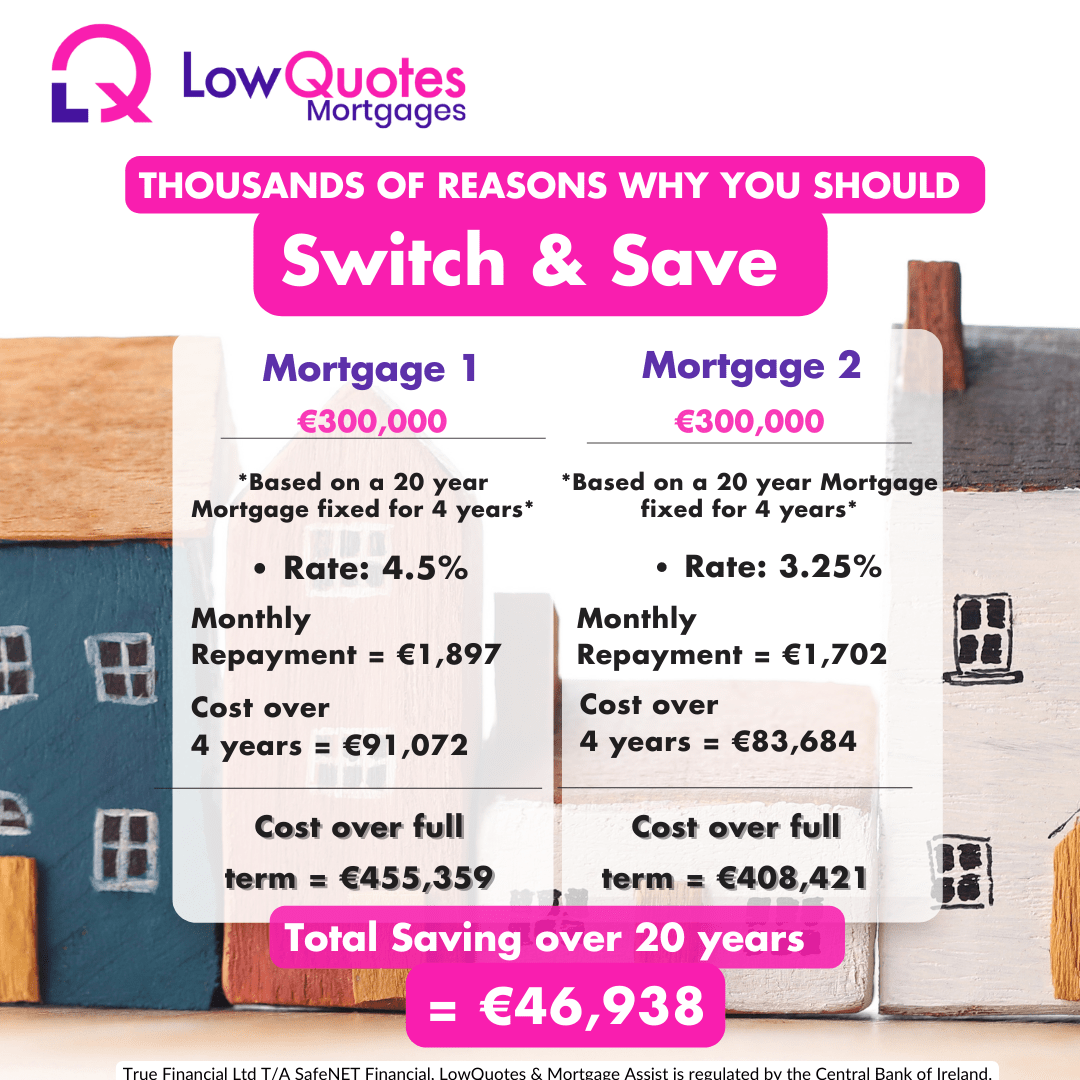

For instance, if you have a mortgage of €300,000 with a 4.5% fixed rate for 4 years and 20 years left to run, your monthly repayment would be about €1,897. The cost over 4 years would be €91,072 and €455,359 over the full term of your mortgage.

If you decide to switch your mortgage to another provider with an interest rate of 3.25% you would be saving €195 per month, €7,388 over 4 years, and €46,938 over the full term of your mortgage.

Note it’s only a difference of 1.25% and it doesn’t sound like a lot but if you put that money into a savings plan over 20 years you could pay for your child’s education, much-needed home renovations, overpay mortgage or whatever you want as it is your hard-earned money.

You also can use the money saved by switching your mortgage to top-up your pension to retire earlier or receive a larger pension upon retirement.

For example, if you contribute €195 net per month into your pension, with tax relief this would be a €325 gross contribution to your pension. By saving this extra amount of money over 20 years you would have an extra €135,000 in your pension pot (considering a 5.1% sector average annual rate of return).

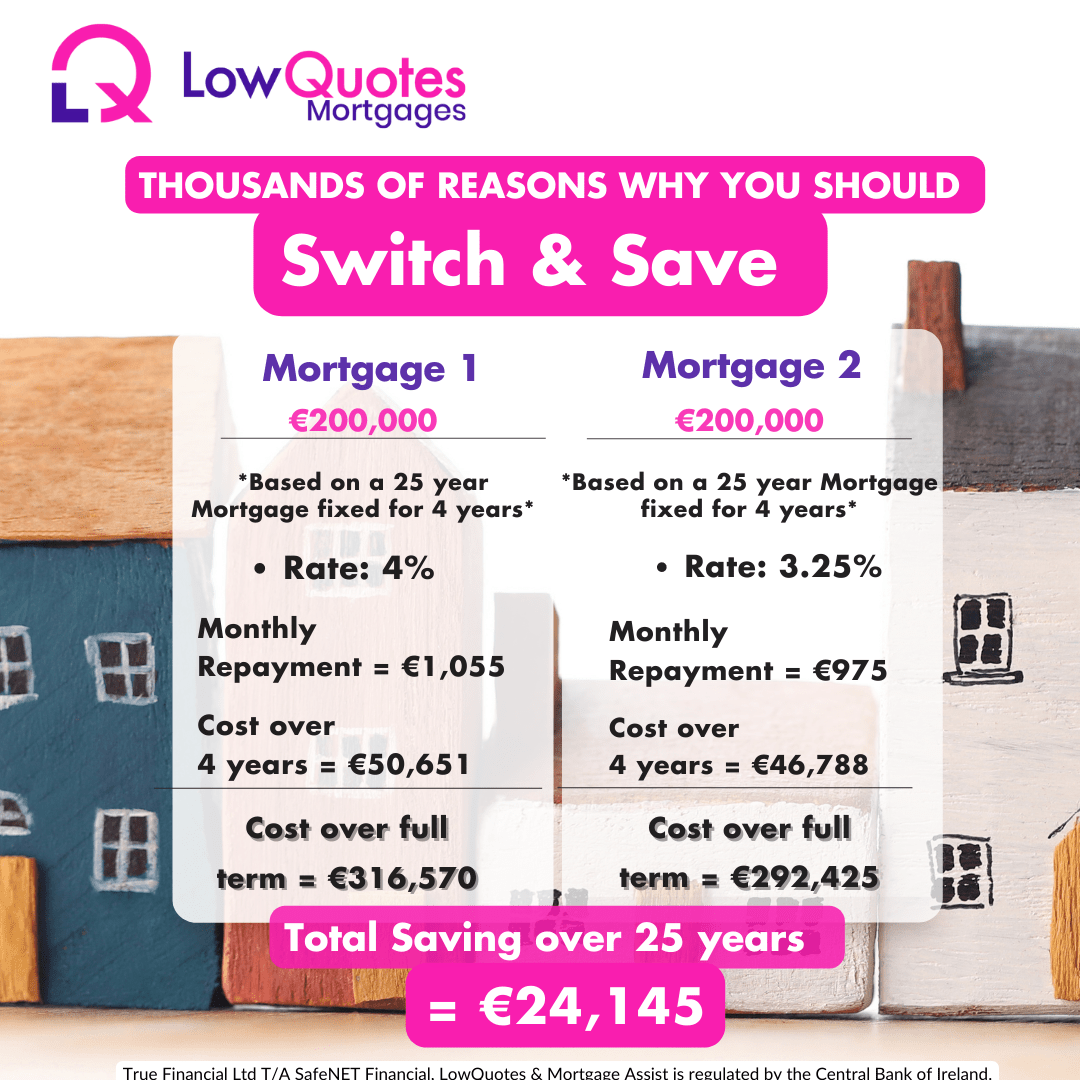

Another example:

Reasons why people don’t switch their mortgage

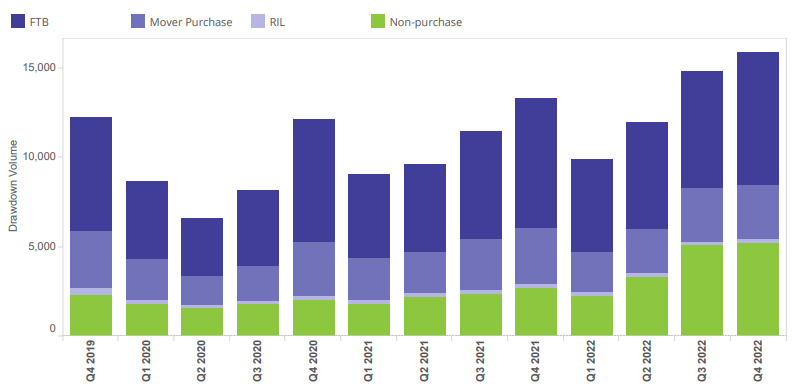

We can observe on the chart below non-purchase (switching and top-ups) mortgage drawdown volumes rose by 124.3% year-on-year to 5,199.

The BPFI report for January 2023 shows that despite a 2.1% increase in volume, non-purchase mortgages (switching and top-ups) approvals have slowed significantly from prior periods, according to the data. This shows that people are missing a huge opportunity to save money by switching.

There are many reasons why people might hesitate to switch mortgage even if they think they could save money by doing it.

Lack of knowledge on how switching mortgage works

Some people might be hesitant to change their mortgage because they are not sure what the process will involve or how long it will take. They might think there is a huge amount of work involved however Switching mortgages with LowQuotes is a very simple process.

The duration of the entire switching process will vary depending on a number of factors such as your application, the lender and their requirements, and solicitors. But in general, around 6 weeks is an accurate estimate.

If you want to have an idea of what you could save by switching your mortgage each month, try out our Mortgage Switching Calculator.

It’s too much effort

Firstly, if the person had a negative experience with applying for their first mortgage with a bank, switching can be intimidating and overwhelming.

Also, some people might think switching mortgages is time-consuming because it requires research and comparison of different lenders and rates. It involves a lot of gathering information and analysis to find the best option.

With LowQuotes, the process of switching can be smoother and less daunting than people anticipate. We compare multiple lenders for you saving you the hardship of visiting multiple banks. All you need to do is provide some quick details and book your switching appointment with us. We will find the lowest rate available so you can make significant savings on your mortgage.

Our state-of-art digital mortgage portal makes it possible for you to switch mortgages while being at home. You can upload your documentation and get approved for a new mortgage from within your portal, which simplifies and accelerates the entire process.