How long do your income protection payments last?

The length of time that income protection payments last will depend on the terms and conditions of your specific policy. Your benefit payment usually stops when one of the following events occurs:

- You return to work after recovery

- You reach the age established in your policy

- You pass away

Can you claim your income protection insurance on your tax return?

You can get tax relief on your income protection premiums at your marginal (highest) tax rate. To know more about tax returns you can get from your income protection contact one of our financial advisors.

If you are a member of a group scheme, your employer usually takes your premium from your salary before tax. In this case, you would not qualify for tax relief as you would have already received the tax relief.

How to claim income protection insurance?

To make a claim for income protection insurance due to illness, injury, or disability, you usually need to follow these steps.

- Check your deferred period to see if you are able to make a claim.

- Notify your insurance provider

- Complete a claim form sent by your insurance provider

- Submit your documentation to support your claim

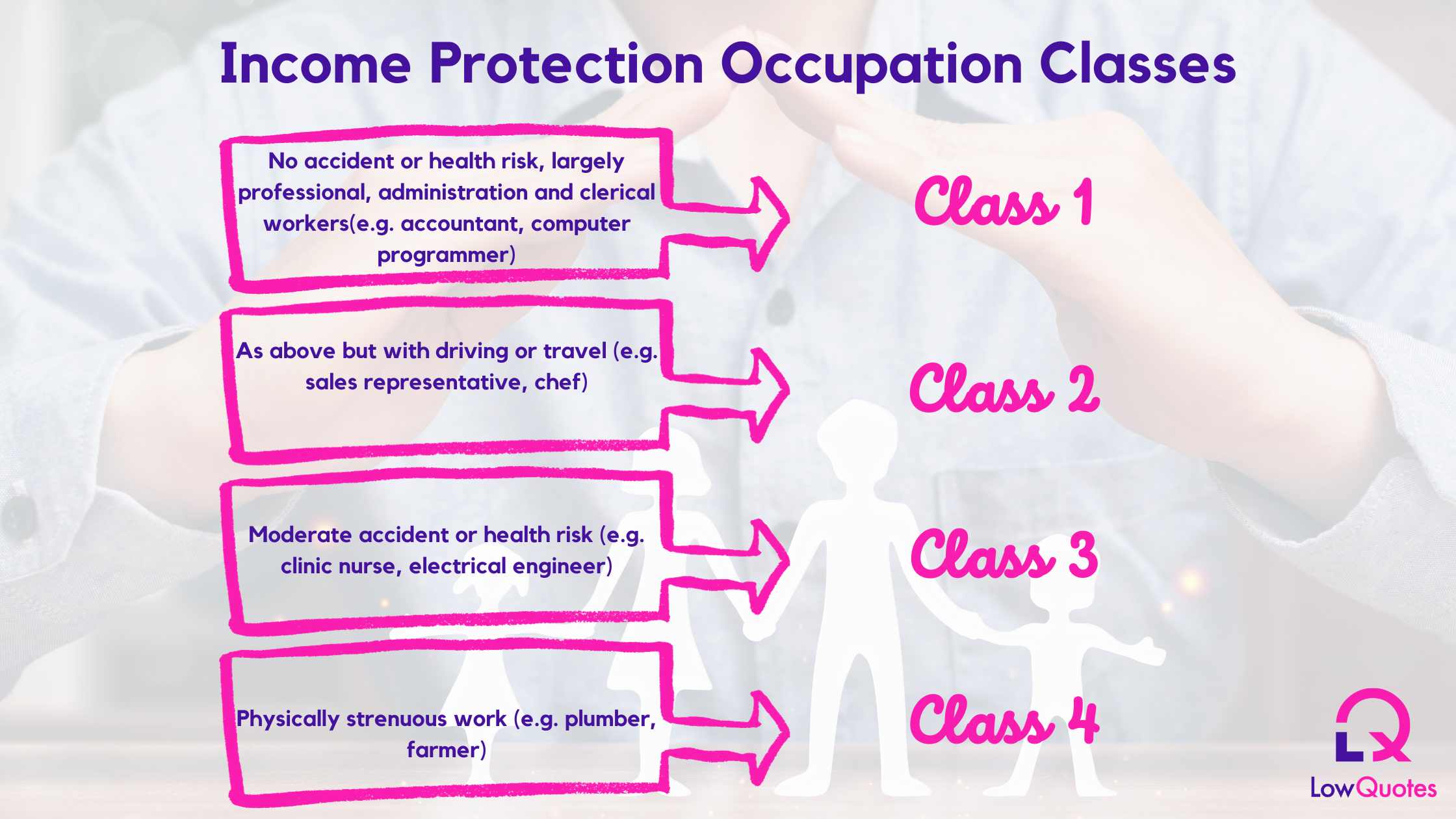

Does your job affect being able to get Income Protection?

Some occupations will not be covered due to the risk factor of the occupation. See below a list of classes and which class you might fall into.

The cover of occupations might vary depending on the income protection provider. To know if your occupation is covered or not, please seek the advice of one of our financial advisors.

Who provides Income Protection in Ireland?

We work with the best income protection providers in Ireland: Aviva, New Ireland, Royal London, and Zurich. Check our income protection calculator and, in a few seconds, find the best income protection quotes.

We compare Income Protection from every provider in Ireland providing you with the lowest quote and best conditions to suit your needs.

Compare Income Protection Insurance with LowQuotes

Low Quotes is an award-winning market-leading online insurance broker with a 5-star Google rating. We compare the best income protection from various providers to find you the lowest quote.

We also provide a wide variety of Financial services such as Mortgages, Life Insurance, Mortgage Protection, Pensions, Financial Planning, and Savings & Investments. If you have any questions about one of our services, feel free to contact us today.

1 thought on “Your Guide to Income Protection Insurance: Answering the Top Questions ”

Comments are closed.