Which one is right for you?

Critical Illness Cover is well-suited for addressing immediate, short-term expenses associated with critical health conditions. On the other hand, income protection is designed to replace your income over the long term, allowing you to continue with your life despite unexpected setbacks.

You don’t need to limit yourself to just one option. In specific circumstances, combining both Critical Illness Cover and Income Protection can offer a more comprehensive level of financial security.

Having both income protection and critical illness cover in place can be a wise financial strategy. These two policies complement each other effectively. While income protection provides you with a regular income stream if you’re unable to work due to illness or injury, critical illness cover offers a lump sum payment upon the diagnosis of a specified serious illness. By having both policies, you create a comprehensive safety net for your financial well-being.

Income protection ensures ongoing financial support for day-to-day expenses, while critical illness cover provides a substantial payout to cover immediate medical costs or lifestyle adjustments. This dual approach can offer valuable peace of mind, knowing that you have coverage for various scenarios and potential financial gaps.

Reach out to one of our financial advisors for personalised guidance.

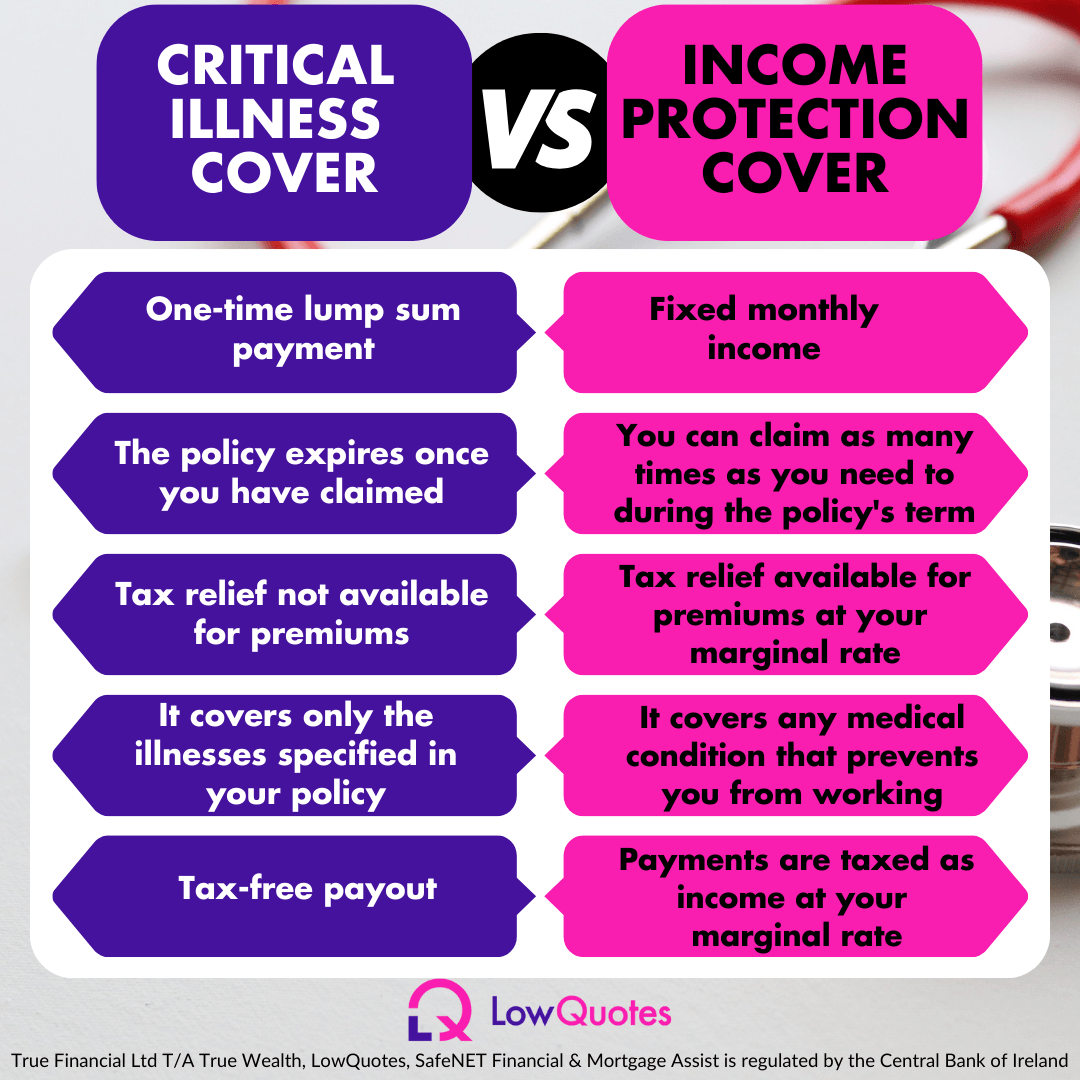

To help your comprehension of the distinctions between critical illness and income protection, let’s outline the key variances between the two:

Practical Examples:

Example 1: Income Protection

Sarah had been working as a software developer for five years, enjoying a comfortable salary and a fulfilling career. However, she never expected to be diagnosed with a serious medical condition that required her to take an extended leave of absence from work. Fortunately, she had wisely invested in income protection insurance.

When Sarah’s illness forced her to stop working, her income protection policy kicked in, providing her with a monthly benefit equal to 75% of her pre-tax income. This financial support allowed her to cover her mortgage payments, utility bills, groceries, and other essential expenses while she focused on her recovery. Without the income protection policy, Sarah would have struggled to make ends meet during her illness, but thanks to it, she could concentrate on regaining her health without worrying about her financial stability.

Example 2: Critical Illness Insurance

Cormac was a self-employed graphic designer who had always taken good care of his health. However, life can be unpredictable, and he was diagnosed with stage III lung cancer, requiring extensive medical treatment. Cormac had wisely purchased a critical illness insurance policy several years earlier.

Upon receiving his cancer diagnosis, Cormac submitted a claim to his critical illness insurance provider. Within a few weeks, he received a lump-sum payment of €100,000, which was the coverage amount of his policy. This financial support was a game-changer for Cormac, as it allowed him to cover his medical expenses, such as chemotherapy and surgery, as well as hire additional help for his business during his treatment.

Cormac’s critical illness insurance policy not only provided financial relief but also peace of mind during a challenging time. It ensured that he could focus on his recovery and continue supporting his family without worrying about the financial burden of his illness.