Annuity vs. ARF: What’s the Difference?

You’ll often hear annuities mentioned alongside Approved Retirement Funds (ARFs). Both help you draw income from your pension, but they work very differently.

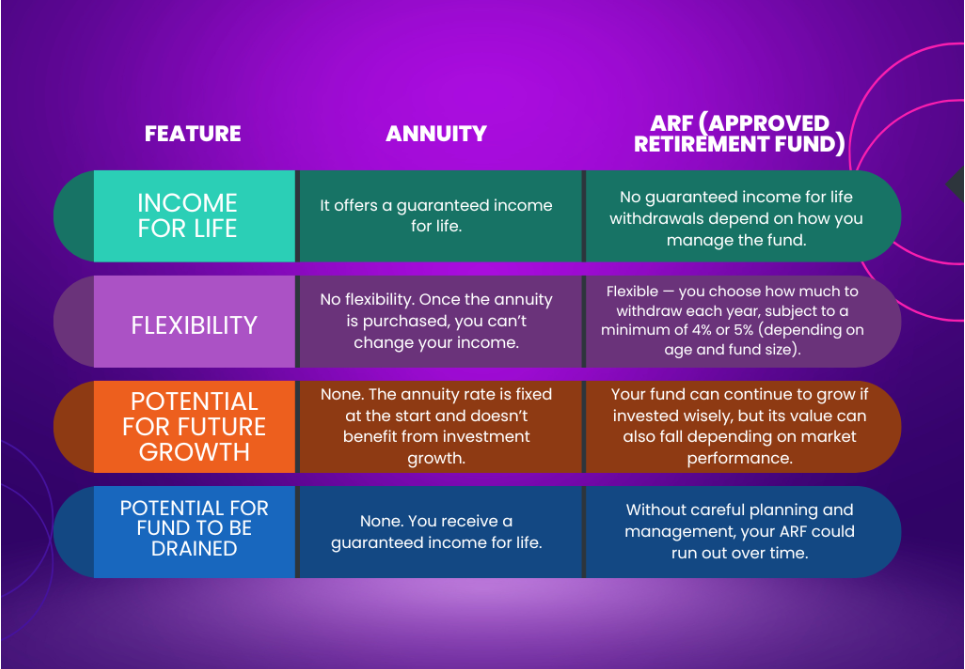

Annuity

- Provides a guaranteed income for life, no matter how long you live.

- Fixed once purchased — you can’t usually change or cash it in later.

- Low risk — the provider assumes market and longevity risk.

- Inheritance is limited — payments usually stop at death (unless you choose a joint-life or guaranteed option).

- You can choose level or escalating payments to manage inflation.

ARF (Approved Retirement Fund)

- Your income is variable, depending on the performance of your investments.

- Offers flexibility — you decide how much to withdraw and when.

- Higher risk, since your fund remains invested and could go up or down in value.

- Inheritance-friendly — any remaining balance can be passed on to your family.

- Growth potential — your fund may increase in value if investments do well.

Who Is an Annuity Best For?

An annuity might suit you if:

- You prefer security over risk and don’t want to worry about market swings.

- You like the idea of a fixed, predictable income every month.

- You don’t want to manage investments in retirement.

- You don’t mind giving up some flexibility in exchange for peace of mind.

It may not be the best choice if:

- You want your pension fund to remain invested and potentially continue to grow.

- You’d like to pass leftover funds to family or beneficiaries.

- You can tolerate market risk and prefer control over your withdrawals.

It’s always best to discuss your personal situation with a qualified financial advisor, someone who can help you understand the tax rules, investment options, and long-term sustainability of your withdrawals.

A Quick Example

Let’s say Mary, aged 65, has a pension pot worth €300,000. She takes her 25% tax-free lump sum (€75,000) and uses the remaining €225,000 to buy an annuity.

She chooses:

- A single life annuity

- Level payments (no yearly increases)

- A 10-year guarantee period

Mary receives about €13,000 per year, guaranteed for life. Even if she lives to 95, those payments keep coming. If she passes away within 10 years, payments continue to her estate until the 10-year mark.

Mary receives about €13,000 per year based on current annuity rates of around 5.5–6% for a 65-year-old purchasing a single-life, level annuity. Actual rates depend on age, health, and the options you select.

That’s the security an annuity brings; no matter what happens in the markets or how long she lives, her income is protected.

Tax and Income Details

In Ireland, annuity payments are treated as taxable income, just like a salary. That means income tax, USC (Universal Social Charge), and PRSI (if applicable) may apply.

However, you can still benefit from tax credits and allowances that reduce the overall amount you pay, such as the Personal Tax Credit, the Age Tax Credit (from age 65), and the PAYE credit if your annuity is paid through the PAYE system. Depending on your total income, you may also qualify for exemption limits or other credits.

Before buying, it’s worth reviewing your tax position, especially if you have multiple income sources in retirement (like the State Pension, rental income, or ARF withdrawals).

A Practical Checklist Before Buying an Annuity

- Compare rates from several providers; annuity rates vary widely.

- Check if you qualify for an enhanced annuity (health conditions, smoker status, etc.).

- Decide between level or escalating income.

- Consider joint life and guaranteed period options for peace of mind.

- Review how your income fits with other sources (State Pension, ARF, savings).

- Speak to a financial advisor before committing. Once you buy, you can’t undo it.

Looking for More Guidance?

We’ve created The Essential Guide to Pension and Retirement Planning, a clear, easy-to-follow resource that walks you through everything from building your pension to managing your income in retirement.

We also have two helpful articles if you’re nearing retirement:

Alternatively, you can always speak with one of our financial advisors.

They’ll help you understand your options, compare what’s best for your situation, and build a plan that fits your retirement goals. Whether you’re five years away or already retired, having expert guidance can make all the difference.