Remortgaging is the process of getting a new mortgage on the house you currently own, to pay off the existing mortgage and replace it with a mortgage that has more favourable terms; for example, to reduce your interest rate or even lower your term, with the added advantage to borrow additional money against your property (this is known as an equity release). You can negotiate a new deal with your current lender or start again with a new lender.

It means that you’ll stay in your existing home and use the equity you have in the property as security for the mortgage. You might want to raise some money for home improvements, debt consolidation, release equity, pay for education or other once off life events be they expected or unexpected, or simply avail of lower rates.

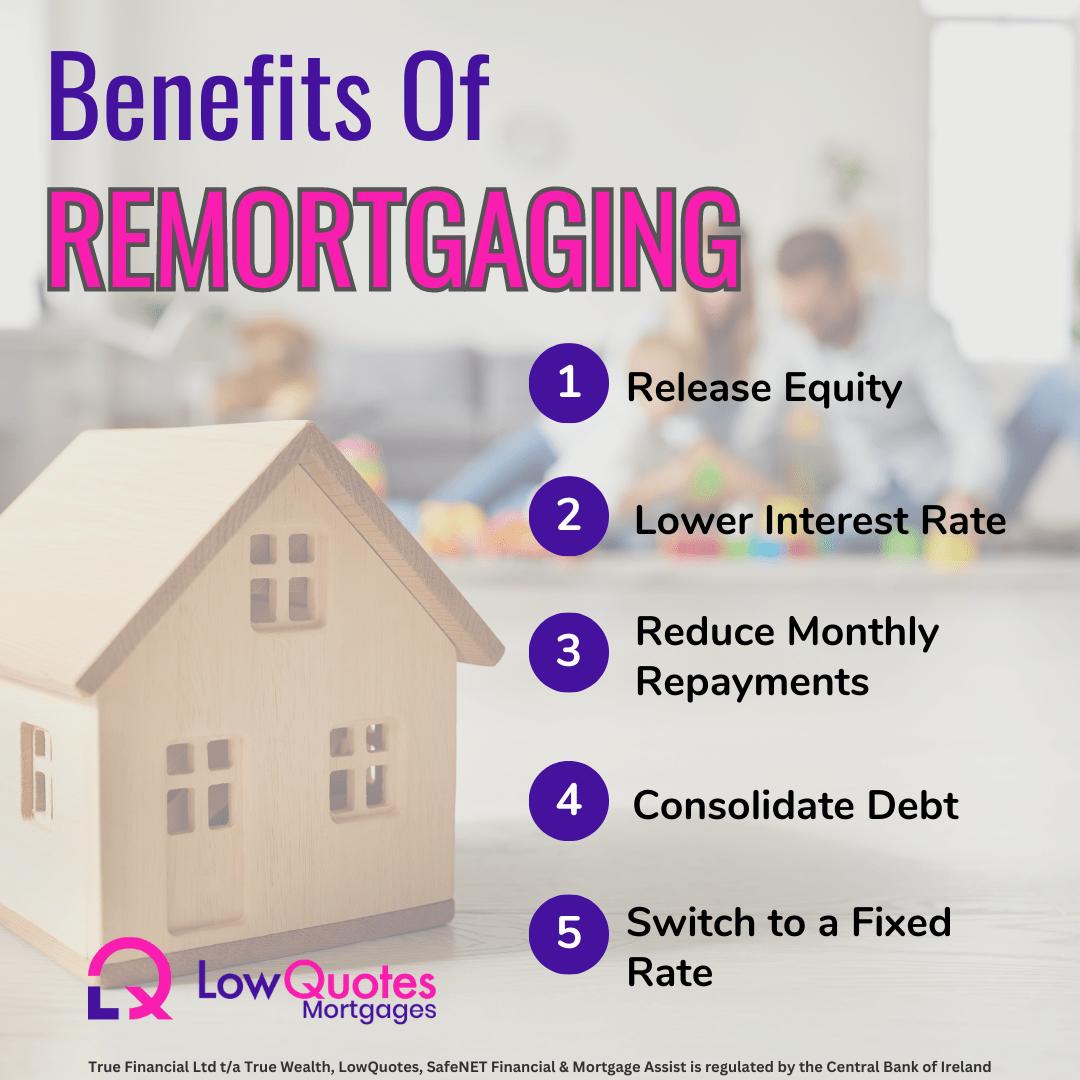

Here are some of the most important benefits of remortgaging in case you are still unsure.

Remortgage to Release Equity

Imagine the following scenario: you have a lovely house but you lack the extra money to build an extension, pay for your children’s education, or consolidate your loans in order to reduce your overall monthly payment, etc.

If you’re in need of extra cash but don’t want to sell your house, remortgaging can be a viable option. By remortgaging, you can release equity in your property and access the money you need without selling your home.

If the value of your home has increased since you purchased it, remortgaging allows you to access the equity you’ve built up. By refinancing your mortgage for a higher amount, you can release a lump sum of cash.

When compared to borrowing through other ways, making use of your equity may allow you to save money as you may potentially pay less in interest.

Lower Interest Rates

One of the main reasons people choose to remortgage is to secure a lower interest rate by fixing their mortgage rate.

Remortgaging could save you a significant amount of money if you are on a variable rate so if you haven’t remortgaged yet you’re potentially paying more than you need to.

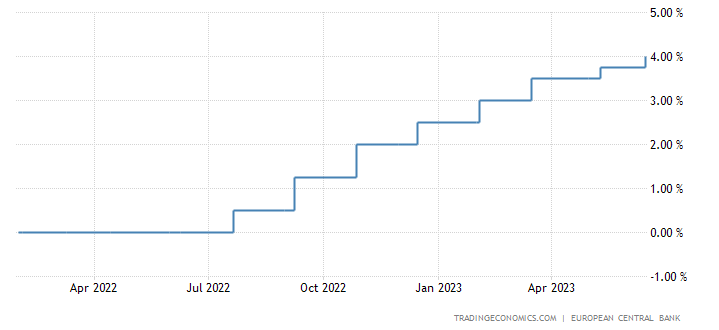

If you have a variable rate mortgage or a tracker mortgage, the ECB interest rates might have a major impact on your mortgage repayments. This is because the interest rate on these types of mortgages is usually linked to the ECB rate, which means that any changes in the ECB rate will be reflected in your mortgage rate. In other words, your mortgage rate will rise if the ECB raises interest rates, which would result in increased mortgage payments.

ECB Interest Rates – April 2022 to June 2023