What is Remortgaging?

Remortgaging is the process of getting a new mortgage on the house you currently own, to pay off the existing mortgage and replace it with a mortgage that has more favourable terms; for example, to reduce your interest rate or even lower your term, with the added advantage to borrow additional money against your property (this is known as an equity release). You can negotiate a new deal with your current lender or start again with a new lender.

It means that you’ll stay in your existing home and use the equity you have in the property as security for the mortgage. You might want to raise some cash for debt consolidation, home upgrades, equity release, education costs, or just to take advantage of reduced rates.

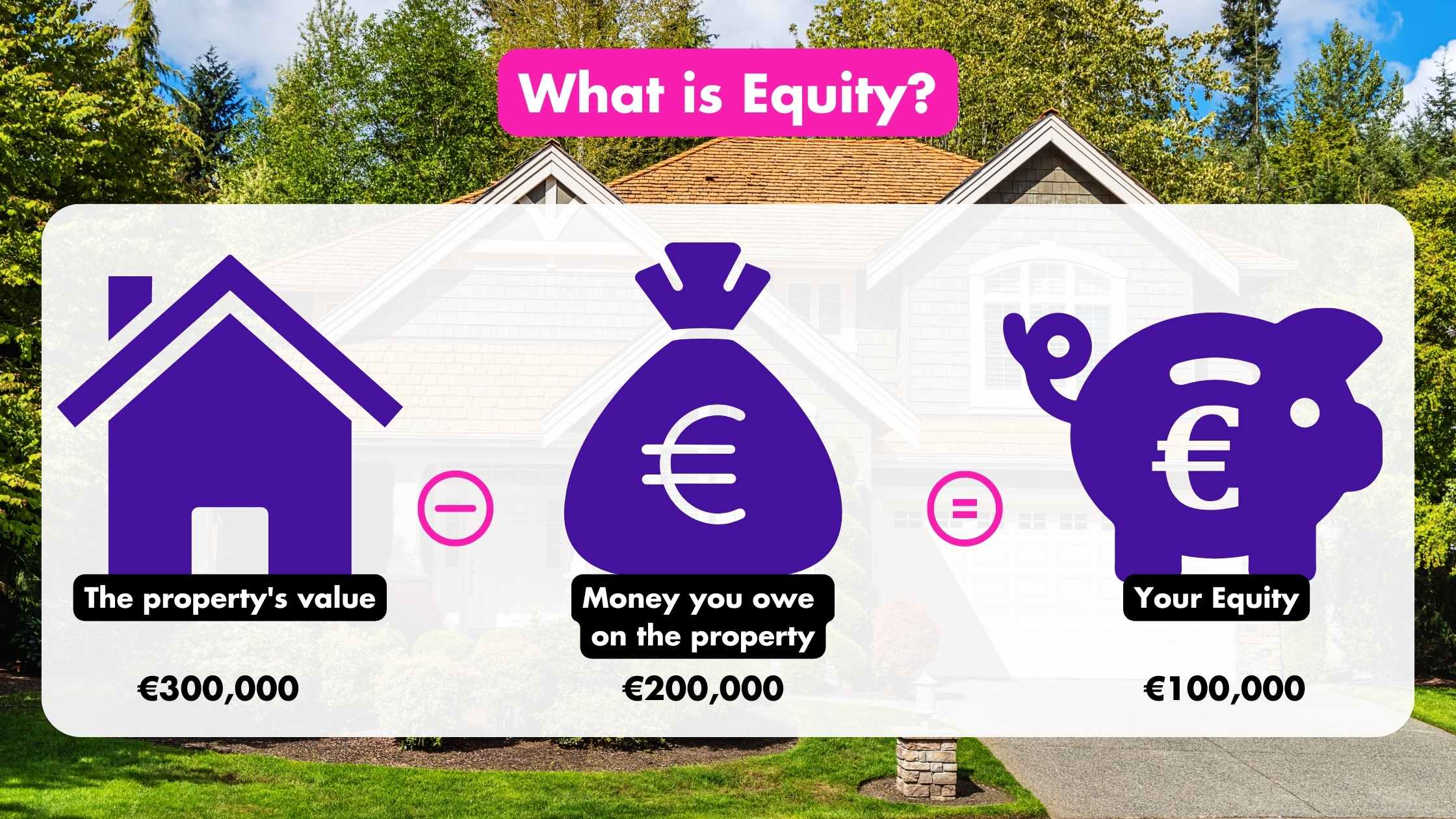

What is Equity?

Equity is the difference between the current value of your house and the amount you owe on it. For example, if a property is valued at €300,000 and the homeowner has a mortgage balance of €200,000, their equity in the property would be €100,000.

What is the LTV rate (Loan to Value)?

LTV is short for Loan to Value. This is the maximum amount you may borrow, based on the current value of the property.

This is a percentage figure which represents the difference between your mortgage loan and the value of your property.

A remortgage applicant can borrow up to 90% of the value of a property, but again, it depends on the lender and their specific criteria.

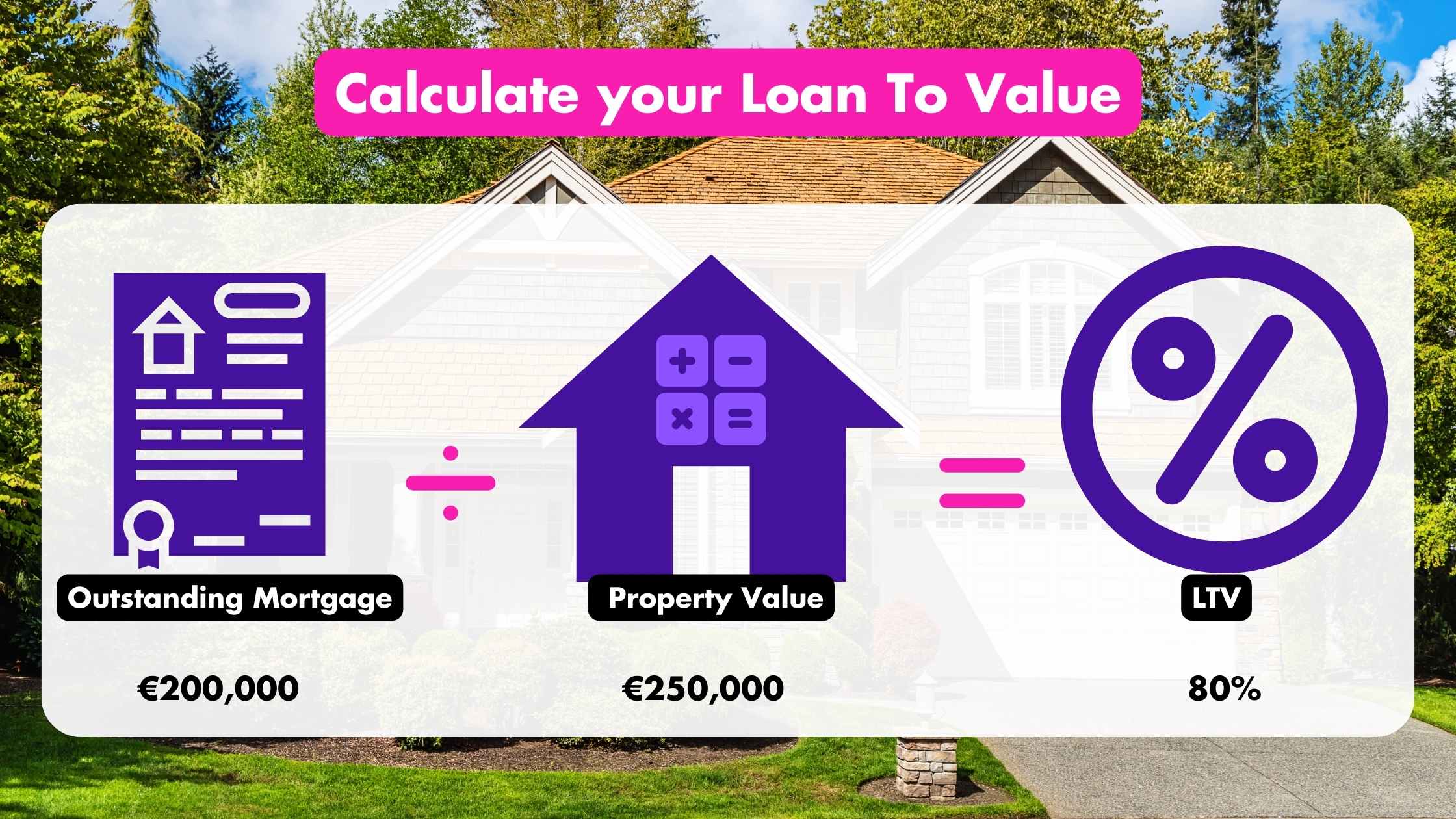

How to calculate Loan-to-Value (LTV)

How Calculating your loan-to-value (LTV) ratio is a straightforward process. To determine your LTV, you need to know the current value of your property and the outstanding balance on your mortgage. Here’s how to calculate it:

Calculate your mortgage’s outstanding balance: To find out how much you still owe on your mortgage, check your most recent mortgage statement or get in touch with your lender.

Find out what your property is now worth: You can determine this through a property evaluation, recent sales of comparable properties in your neighbourhood, or by speaking with a real estate professional.

Calculate the loan-to-value ratio: Divide the outstanding mortgage balance by the current property value. Multiply the result by 100 to express it as a percentage.

For example, if your mortgage is €200,000 on a property valued at €250,000, your LTV rate would be 80%.

How early can I remortgage?

If your mortgage rate is Variable or Tracker, you can remortgage sooner rather than later as Interest rates in Ireland are continually on the rise, at about 4%. So if that’s your situation, it’s definitely worth remortgaging to avoid overpaying. By remortgaging you could switch to a better deal with lower interest rates and lower monthly repayments and avoid further imminent rate increases by the ECB and lenders.

If you started on a fixed rate, and at the end of that fixed rate term your mortgage automatically reverted to a variable rate, then your monthly payments will increase. Remortgaging or switching your mortgage might save you thousands of euros per year by getting a lower interest rate.

We strongly advise reviewing your current mortgage terms and conditions including early exit penalties as well as charges and fees you have agreed to pay in the event you decide to transfer before making the decision to remortgage or switch.

Read more about how much you can save remortgaging/switching in our article.

We also discuss the benefits of remortgaging more in-depth in our article about the Reasons Why Remortgaging Can Save You Money.

What is the difference between a remortgage, a switch, and a mortgage top-up?

Although they all are related to modifying or adjusting your current mortgage, a remortgage, a switch, and a mortgage top-up have different implications and objectives.

Switching mortgages mean refinancing your mortgage with a new lender, while a remortgage can either be with your current lender or a new lender.

A Top-up mortgage refers to a type of loan that allows homeowners to borrow additional funds on top of their existing mortgage, also known as a mortgage equity release.