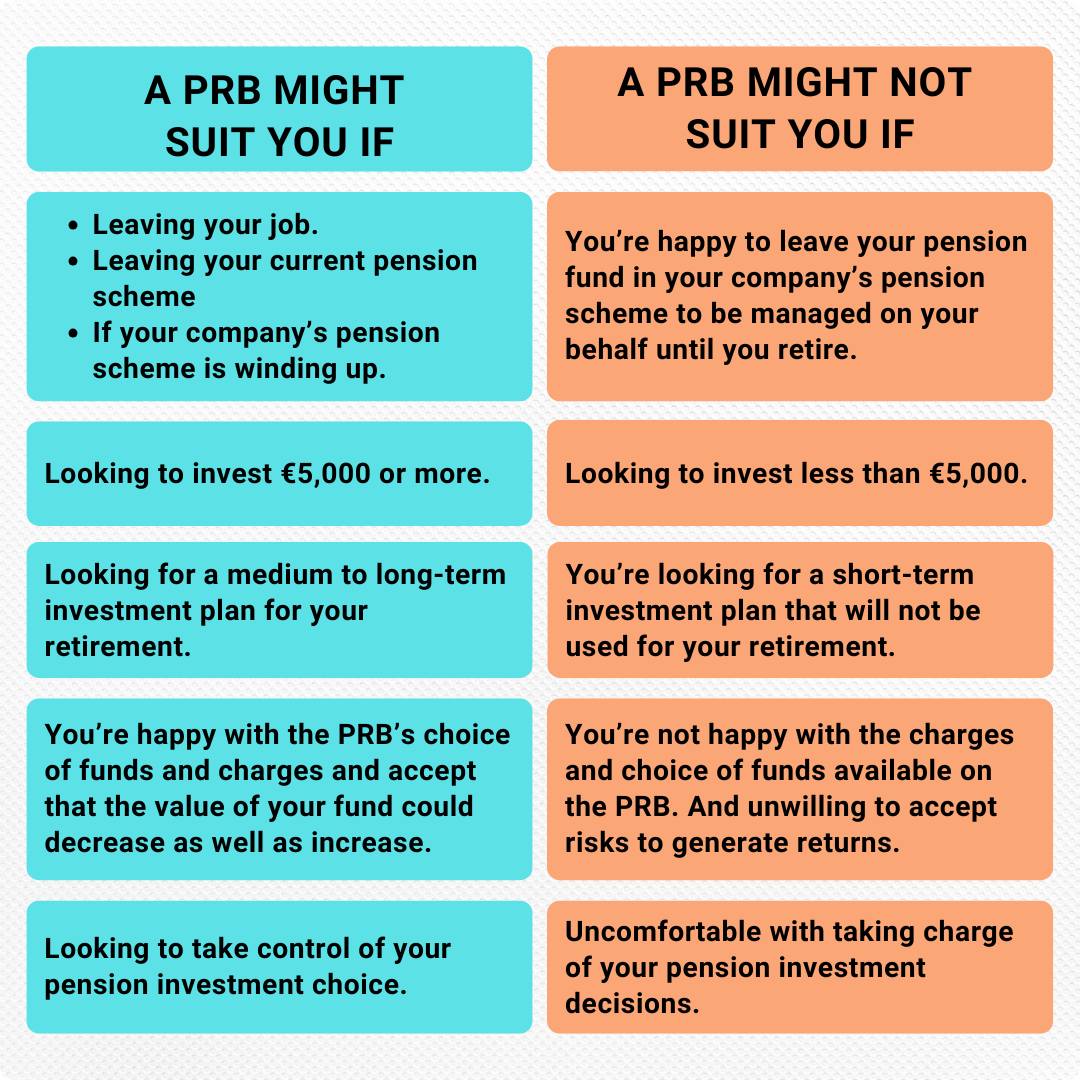

Is a Personal Retirement Bond right for you?

A PRB could be a good fit if you:

- Are leaving a job and have pension savings in your old employer’s scheme.

- Want more say in how and when you invest and access those savings.

- Want to consolidate pension pots (if you’ve had many jobs and lots of different schemes).

- Are comfortable with investment risk (since your money’s invested and its value can go up or down).

But you should ask yourself:

- Do you understand the charges and what you’ll be investing in?

- Are you comfortable tying up the money until retirement age?

- Are you okay with taking responsibility for investment decisions (or working with a good advisor)?

- Are there better options (e.g., leaving the money in your old scheme) that may suit your situation more?

Because everyone’s situation is different, it’s wise to get professional advice.

What Are the Charges?

Like most pension products, a Personal Retirement Bond (PRB) comes with a few different types of charges. These help cover the cost of managing your plan and investments. Here’s a quick breakdown of what to expect:

Fund Charges

The fund charges you’ll pay depend on two things:

- The type of PRB you choose, which determines the plan management charge (PMC)

- The funds you invest in, which determine the fund management charge (FMC)

Together, these make up your overall fund charge. In some cases, you might even receive a rebate, added as bonus units to your policy to reduce your costs slightly.

Allocation Rate

The allocation rate determines how much of your single contribution is allocated to your PRB. For example, if your allocation rate is 98%, that means 98% of your money is invested in your retirement bond, while the remaining 2% covers charges.

A financial advisor can explain the options and help you choose the one that fits your goals best.

Early Exit Fee

PRBs are designed for medium- to long-term investing, typically with a minimum period of around five years. If you decide to move your money or access your benefits early, an early exit fee might apply. You’ll find details of any such fee clearly listed in your policy schedule.

Policy Servicing Fee

In some cases, there may also be a policy servicing fee to cover ongoing administration. If this applies, it will be clearly shown in your policy schedule.

How to Find Pension Funds from Previous Jobs

It’s common to build up pension savings with different employers over the years, and it’s easy to lose track of them. Pension tracing helps you find those forgotten funds and, if you wish, combine them into one plan like a Personal Retirement Bond (PRB).

Our team can help you track down old pensions and make sense of your options, so your hard-earned savings work together for your future.

You can also check out our article on how finding lost pensions could boost your retirement income.

Read Our Articles

We’ve put together plenty of articles to guide you through key financial decisions. You might like the following:

- Why a Private Pension in Ireland Is Smarter Than You Think

- Setting Up a Private Pension in Ireland

- 6 Reasons to Review Your Pension This Year

- 7 Smart Ways to Use Tax Relief to Grow Your Pension in Ireland

- What to Do 5 Years Before Retirement

- The Essential Guide to Pension and Retirement Planning

- Private Pension Myths in Ireland

- Do You Know What Happens to Your Private Pension Plan When You Die?