Life insurance is a vital component of financial planning, offering peace of mind that your loved ones will be supported financially in your absence.

However, inflation is a subtle force that may gradually erode the value of money, which makes it crucial to understand how it affects long-term financial commitments like life insurance.

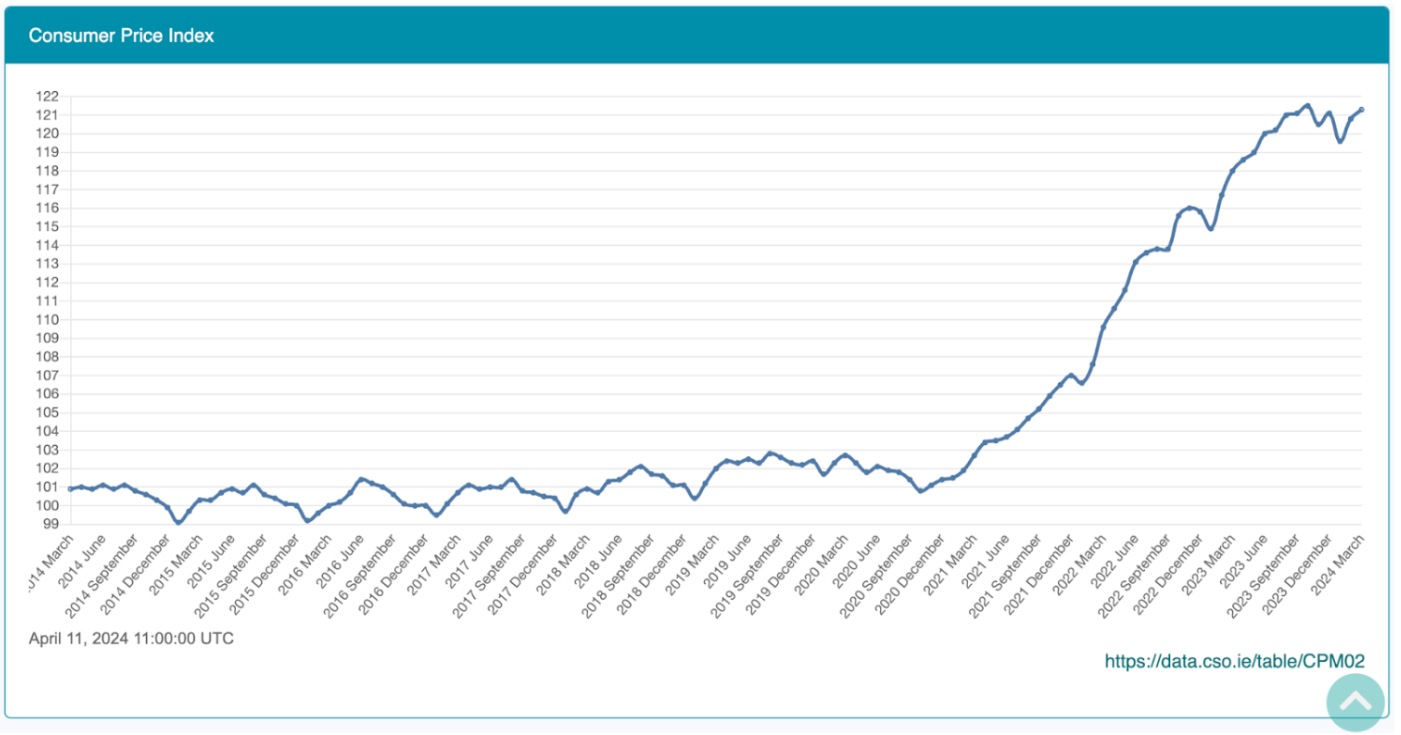

What’s The Effect of Inflation on Money Value?

Inflation is the rate at which the general price level of goods and services rises, subsequently eroding purchasing power.

For someone with a Whole of Life insurance policy, this could mean what seemed like a substantial sum 30 years ago may no longer be enough due to the decreased value of money.

Take, for example, a life insurance policy purchased in 2014 for €200,000. With an increase in the Consumer Price Index (CPI) by 20.3% from March 2014 to March 2024, that initial €200,000 would effectively be worth only €160,000 in today’s money, which is significantly less than originally planned.

This example references the inflation rate from March 2014 to March 2024. It’s important to understand that this is strictly for illustrative purposes, as inflation rates can vary, either increasing or decreasing, depending on economic conditions.

How Can I Protect My Life Insurance Value from Inflation?

When selecting a life insurance policy, you have the opportunity to add various extras, including cover for serious illnesses or a convertible term option.

Indexation is another add-on worth considering, as it helps preserve the purchasing power of your funds against inflation.

What is Indexation in Life Insurance?

Indexation in life insurance is a feature that adjusts the benefit amount over time to reflect changes in the cost of living due to inflation.

This ensures that the value of the life insurance payout doesn’t diminish over time and continues to provide real financial security.

How Much Does Indexation Cost?

Adding indexation to your policy incurs an additional charge, which varies between life insurance providers.

Both the cost of your policy and the amount of cover provided will increase each year. However, the rate of increase in your cover is typically lower than that of your premium.

For example, your coverage may grow by 3% each year, while your premium could increase by 4% annually, which is a typical approach among providers.

Initially, your premiums may seem affordable, with monthly payments appearing low, but it’s important to remember that these will steadily rise over the term of your policy, potentially becoming a significant expense over time.

For a clearer understanding, consult with one of our financial advisors at LowQuotes to determine if this option is suitable for your specific circumstances.