When it comes to life insurance, many people feel relieved once they’ve secured a policy. It feels like a box has been ticked. It may seem like your family’s financial future is safe, however what if your cover isn’t enough? What if you think you’re fully protected, but changes in your life or finances mean the policy no longer fits your family’s needs?

If you purchased life insurance a while ago and haven’t reviewed it, or if your financial situation has changed, you could be underinsured. Here are some signs that your cover might not be enough to protect your family as planned.

Your Policy Was Purchased Years Ago

If you bought your life insurance policy a few years ago, it might no longer reflect your current financial situation. Life changes—such as having children, buying a home, or taking on more responsibilities—often lead to increased financial needs.

Inflation also plays a major role in eroding the value of your policy over time. Inflation is the rate at which the cost of goods and services rises, reducing the purchasing power of money.

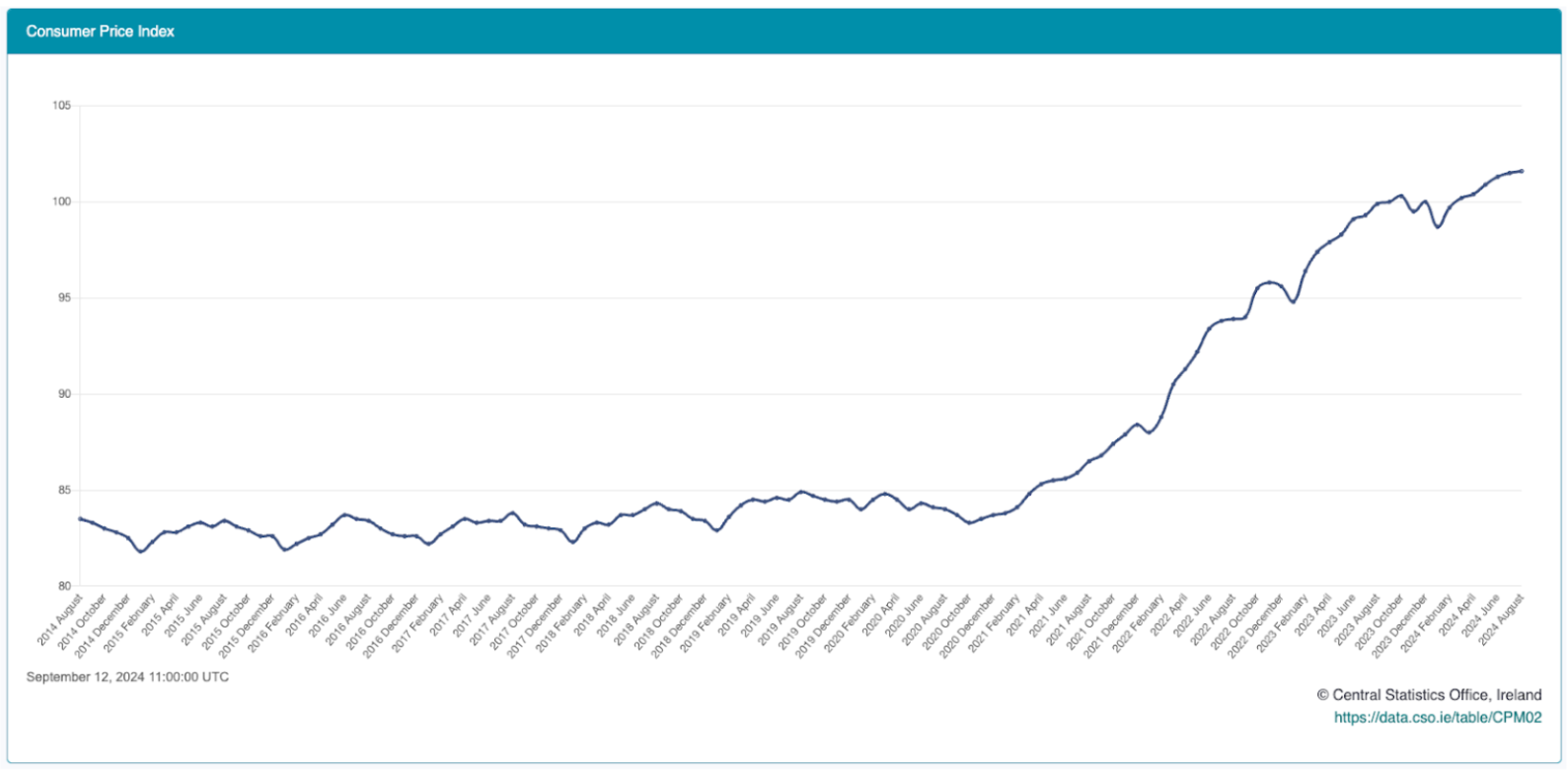

For example, if you purchased a life insurance policy in 2014 with cover of €200,000, and the Consumer Price Index (CPI) increased by 21.7% between August 2014 and August 2024, that €200,000 would now effectively be worth only €156,600.

This drastic reduction in value means your original policy might no longer provide enough cover for your family’s financial security, making it crucial to review and adjust your policy.

This example references the inflation rate from August 2014 to August 2024. It’s important to understand that this is strictly for illustrative purposes, as inflation rates can vary, either increasing or decreasing, depending on economic conditions.

Whether you have term life insurance or whole-of-life insurance, it’s important to review your cover as your life changes. Your family’s needs may grow with new responsibilities or higher expenses, and inflation reduces the value of your cover over time. By adjusting your policy, you can make sure it will still provide the support your family needs in the future.

You can also add an Indexation option to your policy, which automatically increases your cover to keep up with inflation, ensuring it stays valuable and relevant.

Your Stay-at-Home Spouse Doesn’t Have Life Insurance

Many people think only the main income earner needs life insurance, but that’s not true. A stay-at-home spouse provides significant value—looking after kids, managing the house, and more—which would be very expensive to replace.

According to Royal London Ireland, it would cost around €54,590 per year to hire someone to handle all the tasks stay-at-home parents do.

Childcare alone can be a significant expense. The Irish Independent reports that full-time childcare in south Dublin costs up to €18,936 annually, while in Monaghan, it’s €4,080 per year.

Without life insurance for your stay-at-home spouse, you could be underestimating your family’s future financial needs.